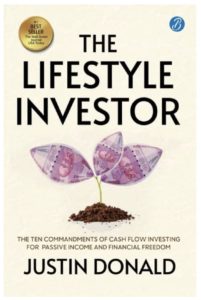

Many people have lost money trying to grow their wealth, but how do you know when an investment is too good to be true? Today’s guest is Justin Donald. Justin is the host of the Lifestyle Investor Podcast and author of the bestselling book Lifestyle Investor: The Ten Commandments of Cash Flow Investing for Passive Income and Financial Freedom. He consults and advises entrepreneurs, executives, and successful media personalities on lifestyle living. Justin has also appeared on nearly 100 podcasts including Entrepreneurs on Fire, The Mike Dillard Show, Making Bank, The Accelerated Investor, and Unbecoming.

“There are incredible opportunities to make money but also to lose money. Not all projects are the same.” - Justin Donald Click To TweetShow Notes:

- [1:02] – Through his company Lifestyle Investor, Justin teaches others how to create a lifestyle that is compelling and purposeful.

- [3:31] – Justin’s mission is to help people buy their time back.

- [4:34] – In many cases, people have lost millions of dollars in poor investment decisions.

- [5:51] – If you want to build wealth, you need to have a strong ecosystem.

- [6:53] – A lot of people in financial services are not in alignment with their clients and the system is manipulative.

- [8:40] – Justin didn’t start out asking specific questions and now he always asks those in financial services.

- [10:02] – You have to do your own work and math to make sure things are not manipulated.

- [11:10] – There are incredible opportunities to make money but also to lose money. Not all projects are the same.

- [13:10] – ICOs are super high risk and Justin advises to avoid them.

- [14:11] – If something is guaranteeing returns, it’s a red flag. There’s always some form of risk.

- [15:26] – Justin admits that he has lost money in situations where he didn’t see the signs in time.

- [17:49] – There are some red flags to look for and Justin shares some examples.

- [21:42] – Having cash flow is important first and then investing becomes safer.

- [23:29] – Almost every business partnership is going to end at some time and 90% or more of them end poorly.

- [25:58] – Always have open conversations and express concerns when making decisions.

- [27:56] – Justin also advises to be careful that you aren’t buying another job and you are looking for passive income.

- [30:51] – What is a targeted return?

- [32:13] – Don’t be lured in by a good targeted return. Justin advises on what to look at instead.

- [34:38] – You want to know how your investments will do if things don’t go according to plan.

- [36:17] – Justin gives an example to illustrate how returns work.

- [37:50] – Justin is offering his book free to listeners by going to his website LifestyleInvestorBook.com.

Thanks for joining us on Easy Prey. Be sure to subscribe to our podcast on iTunes and leave a nice review.

Links and Resources:

- Podcast Web Page

- Facebook Page

- whatismyipaddress.com

- Easy Prey on Instagram

- Easy Prey on Twitter

- Easy Prey on LinkedIn

- Easy Prey on YouTube

- Easy Prey on Pinterest

- Justin Donald Website

- The Lifestyle Investor: The 10 Commandments of Cash Flow Investing for Passive Income and Financial Freedom by Justin Donald

- The Lifestyle Investor Podcast

Transcript:

Justin, thank you so much for coming on the Easy Prey Podcast today.

Hey, thanks for having me. I'm excited to join you, Chris. This is going to be a good time together here.

I'm sure it will. Can you give me and the audience a little background about who you are, what you do, and why you got into it?

They respond to what's happening to them versus proactively planning a life by design that is incredible, where they live their dreams and their goals. They have true vibrancy. The whole purpose of my brand, The Lifestyle Investor, is to teach people they can have a killer life today and they can buy assets that produce income that covers their cost of living, so they don't have to work for money.

They can work because they want to. They can spend their time on the projects that make the most sense for them. But the goal is to really help people buy their time back and not be a slave to money, not be a slave to the income they make, the lifestyle that they have, to the security or safety of a certain role, a certain job, or a certain industry, and really break free of those chains to pursue a life that is really exciting and full of zest and joy.

The goal is to really help people buy their time back and not be a slave to money, not be a slave to the income they make. -Justin Donald Click To TweetI love your mission. It's exciting for me because a number of years ago, my websites have done well enough that I've been able to transition out of full-time work and just do the stuff that I like to do. The podcast that you're listening to now is one of those things that is my way of giving back, sharing what I've learned, and getting up on a soapbox once in a while. I'm trying to help people not to fall for those sorts of scams.

What's cool, Chris, because if you hadn't created the space to be able to carve out the time to just say, “Hey, what do I want my life to look like? What are the projects that really light me up, that I would do even if I made no money doing them?” You may not be having this podcast right now. We may not be having this conversation, but you put yourself in a place to have the time to do things like this that inspire you, that bring you energy. That's really my mission is to help people buy their time back so they can figure out what it is they really want to do and who the people are they really want to spend time with.

My mission is to help people buy their time back so they can figure out what it is they really want to do. -Justin Donald Click To TweetYeah, that's awesome. I think our values are totally aligned in that aspect, and I'm super happy about that. One of the things that you talked about is people living their life reactionary. I see that sometimes when it comes to investing in financial matters. People are just very like, “Oh, I didn't plan on anything happening,” or, “Oh, my friend told me about this great deal; let me jump on it without understanding what it is.”

Yeah. The thing that I hear all the time in what I do, Chris, is I hear it's like nails on a chalkboard. Some of the decisions people make, why they make them, how little research, time, and energy goes into it. In some cases, people just throw their money away.

Chris, I have people that are part of my group and people that I've interviewed for my mastermind or different coaching projects that most people would consider to have enough money to live the rest of their life. But in many instances, they have lost millions to hundreds of millions of dollars.

In one case, we've got someone in our ecosystem that did lose over nine figures of net worth. It's just so important that you're surrounding yourself with people that are experts in the thing that you want to be the thing at. If you want to get into shape, spend time with a fitness coach that looks the way you want to look, not someone that says, “Hey, I'm a fitness coach,” and they don't look that way because everyone today is a life coach.

You’ve got to be careful that you're not taking advice from someone that hasn't done the thing that you want to do. I say this not just from a financial standpoint. A financial is a component of it, but if you want to build true wealth, then it's buying your time back, it's being physically, mentally, spiritually, intellectually healthy, then you surround yourself with people that are doing that. You are inspired by the life that they live, that they lead, and that's who you want in your ecosystem.

You’ve got to be careful that you're not taking advice from someone that hasn't done the thing that you want to do. -Justin Donald Click To TweetYeah, that makes perfect sense. Where are people going wrong in terms of, what are mistakes they are making, red flags that they're making in these decisions in choosing the people in their ecosystem?

A lot of people don't run decisions that they make by other people that have more expertise in that space. That's one easy thing that I see happening. Another thing is that a lot of people in financial services do not have—what's the most polite way I can say this? They're not in alignment with their clients. In other words, a lot of people in financial services and the way that the whole system is right now, it's a broken system, it's manipulative, and Wall Street kind of controls the narrative.

Wall Street makes money whether you do or not and then people on Wall Street get compensated regardless if you do or not, so there is misalignment. People make money when you don't. That is a dangerous place to be because anytime someone can be a money-raiser and get compensated on those dollars, they probably don't have your best interest in mind or maybe I should say there's a good chance that they don't have your best interest in mind.

By the way, I've got a lot of friends in financial services, I've got a lot of friends that are wonderful in this space. Not everyone is like this, but the stats are the stats. Over the last 15 years, only 5% of all money managers outperform just a simple index, the S&P 500 index. Most people pay more for a worse result.

I guess one of the things that I think of is—maybe this is a different explanation—people in the financial services industry get commission and they may get more commission by directing you to order a product or a service that actually isn't in your best interest and isn't the best financial thing for you. That's going to be the challenge. The pressure on them is to do what's in their best financial interest versus you doing what's in your best financial interest.

On top of that, my experience is bad. Most of the things that people in financial services wanted me to get into, they didn't even have their own money in it. That, to me, the bigger issue is you won't put your own money in it but you want me to do it. But you don't know that if you don't ask. That's something at the beginning that I didn't ask and now I always ask it.

Yeah. My wife and I know the financial advisor that we work with. We know the lifestyle she lives, we know her values. She talks about what she invests in. It's like, “OK, I know who you are and why you're making the recommendations you're making. You understand my tolerance for risk, or probably more likely my lack of tolerance for risk. We'll collaboratively be able to come up with what's a good direction for us to go into finances.”

Yeah, and you want to trust someone. Again, there are great people in the space, but there are more people that are not going to get you the result you desire than people who are. Keep in mind, in the last 10 years, the stock market's been on a boom. So if you're not making money in the last 10 years, that's a big red flag. Almost everyone's made money in the last 10 years.

This is something to track and make sure that expectation meets reality. Then there's this manipulation of the numbers that they share and skew them to make them look like they're performing better than they really are. You have to do your own work and do your own math to make sure that it's on the up and up.

We're not necessarily providing financial advice to people—are there particular products and services that a buyer be wary of? Let's say a good one is right now, crypto is everything. “Oh, throw your money in crypto and it's going to double or triple in the next three weeks.” It definitely won't, but that's what you hear people saying left and right. There are definitely significant risks of that. Are there certain platforms, products, and things where, while they may be legitimate investments, people should be wary of?

Yeah. I think that there are two mindsets to go into. Let's talk about cryptocurrency or NFTs. These are the two things that are really booming right now. Even your play-to-earn gaming, we can group into this as well. There's an incredible opportunity to make money, but there's also an incredible opportunity to lose money. Not all projects are the same.

One group of people go in as gamblers. By the way, sometimes that works out. Unfortunately, sometimes that conditions bad behavior, bad habits, and bad expectations of how good someone is at something and later they lose because of just not really recognizing what happened the first time around. You've got other people that go in, they do the research, and they say, “Hey, I actually buy into this strategy or into this utility in this particular cryptocurrency, in this token, or in this blockchain.” In that instance, I think that it can make sense.

At the end of the day, I think there are going to be a lot of crypto projects that fail, that just don't make it just the same way that most businesses don't make it. I think the majority of cryptocurrencies won't make it, but I think the ones that do make it are going to do extraordinarily well. If you get in early—and still, right now, this is early—you can have an incredible return.

Yeah. This is also one of those things that can go to zero.

It can; so can stocks. Part of the reason people invest in mutual funds—and by the way, I don't really care for mutual funds as much these days, but at least an index is that you're getting a grouping, a collection.

Yeah, there's always the risk that things will go to zero, whether it's mutual funds. You’ve got a bigger problem if a mutual fund goes to zero. What should people be watching out for in terms of get-rich-quick schemes, how to identify them, and know what is potentially legitimate, maybe high-risk investment versus, “Oh, this is just a ploy to separate you from your money”?

There are a few things. If we're talking in the world of cryptocurrencies, ICOs, Initial Coin Offerings, those I think are going to be super high risk; really lookout for those. A lot of these do well only for a period of time, the whole concept of pump and dump.

The same thing is true in a company that goes public. Let's talk about a SPAC, for example. You go public and you start at $10. It could go up, it could go down. You may experience some similar things there. Same thing on a new company that just gets listed and has an IPO.

I would say anytime that you have a guaranteed return, you should probably dig in because guaranteed returns are hard to come by. How guaranteed is guaranteed? If everything goes wrong, how are you protected? You can't just have a contract that says, “Oh, it's guaranteed.” “OK, well, how is it guaranteed? What's it guaranteed by? Is there collateral backing it that if this dies, I get the asset that is collateralized, in which case I make my money back?” Anytime something sounds too good to be true, nine out of 10 times, it's too good to be true.

Anytime something sounds too good to be true, nine out of 10 times, it's too good to be true. -Justin Donald Click To TweetLet's define, in your mind, too good to be true. What kind of rate of return starts to get you to question an opportunity?

Anything above the norm and anything where people basically say there's no risk or there's virtually no risk, there's probably some element of risk. There are things you can do to de-risk a deal, and virtually, all deals, there's some form of risk. Anytime I see something that is being projected above the standard of the norm in that industry, my antennas go up.

Anytime I see something that is being projected above the standard of the norm in that industry, my antennas go up. -Justin Donald Click To TweetBy the way, I just want to be open with you and your audience. Part of the reason I know what to look for is because I've lost money. I have made poor choices. I have trusted the wrong jockey. I've had people lie to me.

In my book, The Lifestyle Investor, one of the first things I do is outline where I invested in a Ponzi scheme. I didn't see the signs then, and in some cases, they totally lied so maybe you couldn't have seen them. But today, I see some things I would have done differently, some due diligence items I would have done differently. That was a too-good-to-be-true situation. It was a guaranteed return situation.

There was a contract that was obviously not created by an attorney or a very good attorney. There are just some signs that, unfortunately, I got lured in and I started cashing paychecks that hadn't happened. I looked at the return as a done deal versus making sure I was mitigating a worst-case scenario.

When you say you were cashing paychecks that you hadn't gotten yet, were you talking about, “I see my account balance at the advisor, at the institution, and the entity, is going up, but I actually haven't drawn any of it out.” Is that what you're referring to?

In this case, the company was good until it wasn't good. It actually didn't start as a Ponzi scheme. It was 27 years of a legitimate company and then it became a Ponzi scheme. To a certain degree, it makes it hard—how do you really know?

There are signs, there are cues, and there are tells that you'll learn to pick up on. But in this instance, sometimes it's like, “Oh, you're giving me a 22% return guaranteed.” In my mind, it's like, “OK, I'm cashing this 22%.” I see a lot of people fall prey to this type of thing where they romanticize the amazing return, but keep in mind, the return isn't real. It's a number they put there and it's not a done deal until you get all your money back, until the investment goes full circle. Anything can go wrong at any point in time.

I know there are asset classes where you can't touch your original investment and you can't get your money back out for a certain period of time. Is that something that, in and of itself, is a red flag or is that just a small, depending on what it is, it's a red flag?

Know what RED FLAGS to look for!

It could be a red flag. It depends on the type of investment. In real estate, generally, you're not going to get your money back quickly. One of my 10 commandments in my book, which is my 10 criteria for how I invest, is I do look for my principal to come back quickly. That, to me, is safer because it de-risks the deal. Maybe I don't make the return on those dollars for as long, but if I get it out, then I de-risk the deal and I've got some upside on house money, so I look for that.

There are other deals. There are ways to invest right now. I'll just give you one perfect example that I see a lot of people doing: angel investing. They find a startup and they're like, “Oh, this is great. I believe in this, I believe in the team,” and they invest in this company. But the reality is, we don't know if that company is going to make it.

There's a 96% chance that that company's not going to make it, actually. At that stage in the business—pre-revenue, it's probably 97% or 98% likely it's not going to make it. But you don't know that and you won't know that necessarily for maybe even 10, 15, or 20 years.

In essence, what you've done is you've given your money to a high-risk investment. It's like the equivalent of a 0% interest loan for an undetermined period of time that just doesn't end up working out. It's a poor investment unless (a) you know what you're doing, (b) you've got some insider baseball, (c) you, at scale, have enough of these companies that you only need one to hit and you have enough of them.

Generally, 50 is the magic number in angel investing. If you have 50 different angel investments, probably one's going to hit that's going to cover all the losses, but most people don't have it at scale. Most people invest in this idea that's pre-revenue. In some cases, it's like a pre-product.

It's on a napkin at this point.

Right. That is so high-risk investing, but most people look at that as one of the only ways to invest. To me, that's the last place that I invest. I get all my others. I get my cash flow first, so that way I'm comfortable, I can live my lifestyle, and then I invest in other asset classes that I know are going to appreciate and have a good return. I want to invest in healthcare, and I want to invest in technology. I want to invest in affordable housing, agriculture, energy, original content, music, royalties, cannabis, hemp, CBD, and ecommerce.

There's just so much that you just know it's going to increase and improve like SaaS platforms, subscription platforms, and technology-based. To go in the direction of a high-risk angel investment that most people don't even see as being high risk, or they don't understand that, to me is just crazy. That's way after I get everything else done.

Is it like you operate with a mentality of, “If I lost my entire investment, am I OK with that?” Is that part of your thought process?

Yeah, it needs to be. “Does this put me in financial peril that if I lost it, my life would be massively impacted? That might be too much to invest then?” I do think that that's important. Or if you're going to invest an amount where there could be some impact, maybe scale back the total dollar amount, but maybe invest in something that's a lot safer, that is an asset that holds value, that it's not going to go to zero, so in a worst-case scenario, you're still getting money back.

In most real estate, and especially if you buy cash flow in real estate, it's not going to go to zero. Then if the market tanks but you have cash flow, then you're not worried about what the price is, you don't have to sell it. There are so many ways that you can invest in things where you're protected, where it's safe, where you're not going to lose the value of your money. But yeah, that's got to be in your mind.

In fact, one of my attorneys, one of the greatest lessons I learned from him is to look at every deal as if it's going to fall apart, and then from there, try and play out the story of how it would actually work. Because you're going to make a whole lot of different decisions than if you think, “Hey, this is going to work; let me pick it apart a little bit.” Why don't you just say, “Hey, this isn't going to work, but if it did, here's why it would work, here's how it would work, or here's what would need to happen in order for it to work.”

Yeah, it reminds me of a friend who was going into a business. It went south, and extricating himself out of it was just this huge nightmare. He came away basically saying, “The lesson I learned was it's really easy and sexy to get into business with somebody, but what no one ever talks about is if this deal goes south, how do we both get out of it without hating each other?”

No one spends time working on the exit clause. They think about the profit-sharing, how are we going to make millions together, but no one thinks about if this goes bad, how do we get ourselves out of this?

We could do a whole episode, Chris, on just business partnerships and how those go bad. The reality is, almost every business partnership is going to end at some time, and 90-plus percent of them end poorly because the way that things start is not the way they end, and money is a magnifier. Money magnifies who people really are.

Money is a magnifier. Money magnifies who people really are. -Justin Donald Click To TweetThere's a certain amount of a facade that people can have, but the ultimate magnifier when money comes into play is going to bring out people's true colors. Unfortunately, in many cases, you're going to see something that you don't care for as much or that maybe you didn't even realize was there. These are things I think are important to unpack.

We're talking about prey or being wary. Be wary of business partnerships. When they work, they can be great, but I would go into those knowing that at some point, it's not going to work. Think about divorces. I think we're somewhere at a 50/50 staying married and staying divorced. On the business side of things, it's like 90/10.

Most business relationships end and they end poorly. You want to think through that and make sure that you're in alignment right out of the gate. Make sure you discuss all this stuff on the front end.

Yeah, and not that I want to go a total segue […] businesses, but even the whole thought of like, “One of the business partners die; how is that handled?” No one thinks about that until someone's in the hospital and it's too late.

Yeah, I agree. All of these plans need to be thought through before documents are signed. All of this really should be addressed in the operating agreement.

Yeah. But people getting into business haven't always been in business before. Unfortunately, I think, I've learned this and you've probably learned this. You learn a little bit through the school of hard knocks by doing something, it falls apart, it's really messy, and you go, “Oh, I don't want to do that again.”

Yeah, that's exactly right. You're going to learn great lessons one way or the other. I would just pick your business partners wisely and have open, transparent communication about concerns, fears, everything, and it's likely going to work out a lot better. I don't want to scare people out of going into business because of such a high breakup rate, because there's a lot you can learn in the process even if you do end up breaking up.

Yeah. There are some things that I've done that have gone horribly awry and been a total failure in the sense of the business aspect of it. But the lessons I learned, the processes that I learned were worth the financial cost of the experience. It's like earning an MBA. You can either pay your school or you can pay it out in the business losses.

That's right.

Maybe that's not a good comparison. When things go south, you could definitely learn a ton from it.

You just have to learn your lessons because the money is gone, the time's gone. So if you don't learn the lessons, then that's the atrocity of it all. If you learn the lessons, then that's great. Then next time around, you're better prepared, and you'll likely serve your time and your finances better.

Is there another lesson that you've learned from your personal experiences, investing, and trying to enjoy your lifestyle where you realized after the fact, “Oh my gosh, that was a huge mess. I should have X, Y, or Z”?

Oh, gosh. I could give you a laundry list of stories. One of them is buying a job. One way that a lot of people invest is they like to buy a business or they like to buy real estate, but that business or that real estate can end up owning them. I see this happen all the time. Someone transitions from a corporate job to passive income, then they want more passive income, and they keep adding passive income to the point that that becomes its own business that then runs them and they've lost the passive aspect of that income. It becomes active income and they're tied to it.

I think you’ve got to be really careful that you're not buying a job. From an investing standpoint, if you're looking to transition from a corporate gig—maybe you're an employee, you want to become self-employed, I don't know what the situation is—but maybe you want to pivot and you're OK spending that time, I think that's great. That's where I was, where I was willing to spend time in real estate rentals. For me, specifically, it was mobile home parks. That trade-off of time made sense.

Today, I wouldn't do the same thing, though. Today, I value my time differently. Today, I'm not trying to replace the income from another business to cover my expenses. That's done. The difference today is I don't want to spend more time. I'd like to invest so that my capital alone works and my time is reserved for people that I love. But so often I see people buy businesses, start businesses, invest in real estate, where they own it, their name is on the deed, and it ends up owning them.

I would say the same thing with my business for many, many years. The amount of time that I would spend on it every year would just get a little bit more, a little bit more, a little bit more. It's like, “OK, I'm not doing this right. Yeah, I'm making more money, but I'm obviously not doing this right because the job is running me, not me running it.” Over the last couple of years, I've figured out how to learn how to delegate more stuff and work smarter, not harder. That has definitely freed up time for me to do things like the podcast.

That's right. That's amazing when that happens. When you can find that space, when you can truly buy your time back, and you can focus on what it is that's going to bring you the most joy, that's an incredible place, because I saw something—I actually posted this on social media. It's basically the difference between rich people, wealthy people, and there was a picture of a gold watch where someone owns a gold expensive thing, and then there's a picture of a watch that isn't gold. It's just clear, there's no color to it. But in that example, that person owns their time. That's the difference, who owns your time?

Yeah, I definitely like to be in the position of owning my time and being the master of my time. It is a very nice position to be in, and I'm very grateful for that. There's one other thing that I occasionally hear in investment commercials, and I figured I'd run it by you because maybe it is also a warning sign—when companies talk about targeted returns. To me, it's like, “Are you trying to pretend that you're guaranteeing it, but you just don't want to use the word guarantee and you're just throwing a big number out in front of me?”

This is going to be par for the course. People are going to say, “Hey, here is the return that we project or that we target.” Keep in mind that that means nothing. You can't get your hopes to the fact that that's what you're going to earn. People sell you on their investment by having a higher targeted return. The targeted return doesn't mean anything until it's full cycle and you see what the return is.

The better question is, “What was your targeted return on your last deal?” Meaning, “What was your pro forma? What was it like, everything went to plan, and how far off from that were you?” That, to me, is the better question because a targeted return means nothing. Hey, you can gauge what you think it's going to be, but that means truly nothing. It may come above it or below it. There's nothing to say that that number is going to work out.

In some cases, they could have a plan of why it may work out, but in other cases, you're saying it could just be they just pulled the number out of the air and that's what they're hoping and praying for.

Everyone has a plan. Then what happens when things don't go to plan? Anytime I see a targeted number, most people get lost in the allure of a good return. I would rather say, “OK, in a worst-case scenario, what happens? Do I lose my money? Do I lose part of my money? Do I lose all my money? Do I lose none of my money?” “Oh, OK, so this is safe, this is secure, it's collateralized.”

I can't lose any money, and my return, maybe it's not the sexiest return out there. But if I can't lose money and I can earn a decent return, great, that sounds awesome, sign me up. Most people go for the great return but there may be a lot of risks. It may not be a situation where they're going to get all their money back if something goes wrong.

Yep. I suppose another trap that people get into is thinking that just because something had a good return at one point or just because it did well in the last 30 days, it's going to continue to do that for the next 10 years.

Yeah. Keep in mind, everything has had a good return for the last 12 years. If you have invested in something in the last 12 years and it didn't work out, it must have been really bad because it is hard to lose money in this cycle when you print this much money. When 40% of the dollars in circulation were created out of thin air within the last two years, all asset prices are going to increase at the same rate as monetary supply increases.

You really would have to work hard to lose money on an investment. Even people that are unqualified, probably shouldn't have their own syndications, made money. They have no track record, no experience, and the only time they've ever done it and they posted a huge return.

I like to look at the track record much beyond that. I want to see someone that's had a 20-year or 30-year track record. I need to know they've at least gone through the 2008 financial crisis. I want to know what the results look like. I want to know what they learned. Did they lose money? Did they not lose money?

Ideally, if they went through the dot-com bubble, I just want them to have gone through rocky times and I want to know how they responded. I want to know how their business did. I want to know the pivots that they've made. But if someone's only been around for a decade, that doesn't mean anything to me. Everyone's made money in the last decade.

I think that goes back to what you were saying before: I want to know what's going to happen when things don't go as expected.

Yeah. Because ultimately, that's what's going to happen. No deal goes to plan. That's all I'll say. No deal goes the way that it's supposed to go.

Not even my money market account earning 0.1%?

If you've been in the stock market, it's been good for you. But if you were in the stock market at the time of COVID where it dipped 30% and then you got back 30%, most people are like, “Oh, yeah, it's a wash. I'm back to even.” No, you're not. You lose 30% and then you gain 30%, which means you're negative.

If you had money in the financial markets in 2008, 2007, right in there, 2009, so much was lost then that it takes a long time to get that back. Truly look at what was the total amount of money you've put in, what is it worth today, what was your real return, and divide that by the number of years. It's going to be a different number than what they put on your statements to keep you giving them more money.

Yeah. Always follow the money.

Yeah. Just for simplicity's sake, you have $100,000, the market tanks, you lose 50% of your money. Think about the financial crisis. This is not an unreal situation. You lose half of your money. You go from $100,000 to $50,000. You lost 50%, but what if you gain back 50%?

Yeah, $75,000.

Seventy-five thousand not $100,000. Your average return is 0—a -50 and a 50, so your average rate of return is zero, but your actual return is -25%.

That's rough. As we're winding up here, any parting advice and where can people find you online?

My parting advice is to find a group of people that this is what they do and they know investing, they have a track record, and they do what it is that you ultimately want to do. The five people you surround yourself with and spend the most time with are the people you're most likely going to become. We've heard this over and over, I believe, originally from Jim Rohn, maybe someone even before Jim Rohn that you're the average of the five people you spend the most time with. That's true.

The five people you surround yourself with and spend the most time with are the people you're most likely going to become. -Justin Donald quoting Jim Rohn Click To TweetGet a mentor in some way, shape, or form. Get a coach that is doing the thing that you want in whatever area of life it is. If it's in finances, find someone that is living that life that wants to pour back in a way of coaching or mentoring. That would be my biggest advice.

There are a few ways that you can find me. If you want to read my book, it's called The Lifestyle Investor. For your audience, I'm going to give it for free. They just have to pay for shipping. If you go to lifestyleinvestorbook.com, that's where you can get that for free.

You can, of course, get it on Amazon or wherever else. All the proceeds of that book go to charity. All of them go to a group called Love Justice International. They stop human trafficking in over 20 countries around the world. They're absolutely incredible. You can get that at lifestyleinvestorbook.com.

If you want to learn about any of my other programs or groups, you can check out my website, justindonald.com. There, I've got a blog. Obviously, that's free. I've got a podcast as well, so a lot of free info, and then I've got an online course, a master class. I'm rolling out a new mobile home park course that is an extension of the mastermind. We also have a mastermind, a group of just 100 amazing people. Those are the main programs and products that I have that people can look into if they have an interest.

That's awesome. We'll make sure to link to all those in the show notes. Justin, thank you so much for coming on the Easy Prey Podcast today.

Thanks, Chris, for having me. It was really fun talking, getting to know you, and learning all the cool things that you're doing for your audience where you're looking out for them and trying to protect them from predators in whatever industry they're in is. Kudos to you. Hats off to you.

Thank you so much. Enjoy your day.