People used to think fraud was something that happened in the shadows, rare, distant, and mostly affecting big companies. But after talking to PJ Rohall, it’s clear that fraud is evolving fast, and it’s showing up in places most of us don’t even think to look.

In this episode, I sit down with PJ Rohall, Head of Fraud Strategy and Education at SEON and co-founder of About Fraud. PJ’s work is all about staying ahead of scammers and helping businesses and individuals understand how fraud actually works. From synthetic identities and AI-powered scams to account takeovers and refund fraud, he breaks it all down in a way that’s both eye-opening and surprisingly accessible.

We talk about how fraudsters think, what makes people vulnerable, and why collaboration is one of the best defenses we have. PJ shares practical tips, real-world examples, and some of the patterns he’s seeing that everyone should be aware of. Whether you run a business or just want to better protect yourself online, this conversation might change the way you think about trust, technology, and the digital world we live in.

“Even when people know the risks, they still fall for scams. That’s why education and constant communication are key.” - PJ Rohall Share on XShow Notes:

- [00:52] PJ Rohal is a co-founder of About Fraud and Fraud Fight Club, which is our in conference, in-person experience. He started that back in 2017, but his fraud prevention journey started back in 2011.

- [02:45] He began studying finance and business. He had some mental health issues and was open to trying something different when he saw a job for a fraud analyst.

- [06:22] His experience transferred really well into the entrepreneurial journey.

- [11:13] It's in the best interest of everyone to collaborate and share tips and tricks when trying to prevent fraud.

- [13:05] Everybody is open or vulnerable to being a victim of a scam. There shouldn't be a stigma around it.

- [14:51] It's powerful to see even tech savvy people being victims of scams.

- [17:20] How a contextually relevant scam could actually get you.

- [21:16] It's PJ's dream to get outside of his bubble and help educate the community the best he can.

- [23:43] Two-factor authentication codes have changed, because they give warnings and instructions for the consumer now.

- [28:45] People with platforms could get the word out about the risk of scams.

- [34:30] Getting fighting scams to the front and center is a challenge.

- [36:57] Handling calls from people who've lost large amounts of money in a scam. Having a psychologist or people who understand human behavior would really help with this journey.

- [40:39] Banks and financial institutions are starting to think differently about handling these issues.

- [41:05] There's also a lot of technology on the market that's designed for scams.

Thanks for joining us on Easy Prey. Be sure to subscribe to our podcast on iTunes and leave a nice review.

Links and Resources:

- Podcast Web Page

- Facebook Page

- whatismyipaddress.com

- Easy Prey on Instagram

- Easy Prey on Twitter

- Easy Prey on LinkedIn

- Easy Prey on YouTube

- Easy Prey on Pinterest

- PJ Rohall – LinkedIn

- SEON

- About Fraud

- Fraud Fight Club

- PJ@about-fraud.com

Transcript:

PJ, thank you so much for coming on the podcast today.

Absolutely. Thank you so much for having me, Chris.

Can you give myself and the audience a little bit of background about who you are and what you do?

Absolutely. My name is PJ Rohall, co-founder of About Fraud and Fraud Fight Club, which is our in-conference, in-person experience. I started that back in 2017, but honestly, my fraud prevention journey started back in 2011 when I worked as a fraud analyst more on the merchant side.

I worked in fraud operations for about seven or eight years, then co-founded About Fraud just as a side passion project to aggregate some resources and honestly bring together things. You don't study fraud prevention, you really get certifications. You have different levels of expertise, but if you want to learn from reports, podcasts, blogs, they're disparate, so we wanted to put them all in one place.

Along that journey, it became my full-time job. I've also worked on the solution provider side too, so I've gotten to see a couple different vantage points. I'm really excited to be on this entrepreneurial journey. As far as purpose-driven, it feels very purpose-driven with where fraud, financial crime, and especially scams has evolved into in 2025.

I don't think there's any real courses in college of, “Hey, this college is great on fraud prevention courses.” How did you get into the field?

It's interesting. We have on our website universities. Some of them, we just basically list out universities that have certain risk management, fraud management, cyber that bleeds into fraud. There are some things out there more and more probably as we evolve, but not nearly enough.

I got into it. I studied finance and business because I was like, “Well, that could make me a lot of money. That sounds cool.” I had a diagnosed anxiety disorder in OCD, but not a well-managed anxiety disorder in OCD. I'm not managing it well, and then taking a job in Manhattan in finance in retrospect was not the best choice.

I essentially had a nervous breakdown in 2008. I returned home to figure out what is going on with my mind and mental health. Especially as we've evolved into scams and the psychology of scams, it's weird how those things intersected later in life.

I got the support I needed. It's always a management process. Whether you have a diagnosis or not, we all have human minds. Once I felt like I was in a good place to join the workforce, I studied at a pretty good university, good degree, and figured I should put that to use. I realized through that process, I didn't like finance, not what I was doing, at least.

I was open. I guess that's the silver lining there to something new, something different. I saw a job as a fraud analyst with a company called GSI Commerce at the time. They were then shortly after acquired by eBay, and it was called eBay Enterprise. They work with a lot of suites of traditional merchants. This was back in 2011. It was a fraud analyst reviewing orders, seeing if they're fraud, seeing if they're not. I was like, “That sounds different. I don't like fraud. I feel like I should help out there.”

I didn't know exactly what I wanted to do there. I didn't know where that would exactly take me. The only bet I was making was fraud was not going away. Scams were not going away. The way I knew the human mind was a journey. Good, bad—it’s a spectrum. Human beings are always going to be trying to deceive folks to get ahead in whatever way that means, financially or otherwise.

Human beings are always going to be trying to deceive folks to get ahead in whatever way that means, financially or otherwise. - PJ Rohall Share on XI was like, “Well, let me see if I can learn as much as I can in fraud operations and figure out the rest later, because I think the industry will be around for a while.” That was a good bet. Fraud operations—we were talking right before this—it’s not glamorous. When you get started, you're entry level. You're not getting paid a ton. As you move up, of course you can do a little better from a seniority or a financial standpoint, but it's a very much growing area.

Fraud in general is a growing industry, so we're piecemealing together data and tools. The experts, if you're blessed with a good mentor, a good team you're on, that's the best way to learn. They show you the ins and outs, what to avoid, how to go through your investigations. If you want to go to the more analytical path, how to build rules or machine learning models. If you want to go into people management, going that route.

That's how I got into it, and that's how I learned the most. It was working in a fraud shop, as they call it, a fraud prevention shop, failing a lot, and not understanding what I was doing and being OK with that. Those things actually translated really well into the entrepreneurial journey. That's how I got in.

It's neat. I remember back in my youth, I worked at the birth of the internet. I worked for an e-commerce company when you could start buying things online, affiliates, and things like that. I was working on the team that was looking at all the online orders. It's interesting that once you've been doing those things for a while, you just look at an order and it just doesn't feel right.

A hundred percent.

It's not the dollar amount. There's just something that works in the back of your mind. It's really interesting.

Yeah, and all the teams have different things that show red flags, risk scores, and all that. That's exactly what it got to be. You would pull up an order and sure there are things that are glowing red or things that just don't look right, but you could quickly digest and be like, “Nah, this doesn't look good. Buying five PlayStations at the same time doesn't always look great.”

There's always a story. We're actually doing it for a business. We're going to raffle these off for a charity. But most of the time, especially if you ever got on the phone with the actual fraudster, they would make up this elaborate story. “I have five grandkids. I'm going to give each one of them one.” Just going into something a little different.

The hardest part in non-obvious fraud cases is those edge ones because there's plenty of good orders. The business that you're working for is all about making good customers happy. They don't want things canceled for fraud,… Share on XThe hardest part in non-obvious fraud cases is those edge ones because there's plenty of good orders. The business that you're working for is all about making good customers happy. They don't want things canceled for fraud, especially if it's not fraud. You're looked at this cost center, you're impeding growth, you're impeding revenue. Nobody really wants to fund it until the bad thing has happened.

I played a goalkeeper in soccer, and it reminded me of like, “You're the last line of defense. No one really looks to you until something really bad happens.” Just comparing professional and whatever athletic career I had, yeah.

Yeah. You're never remembered for all the fraud you did stop. You’re remembered for that one fraud incident that you didn't stop.

Yeah, unless you find people who get what you do. I don't want to jump too much into about fraud without maybe talking about some other things, but our community is about connecting with like-minded folks, people who get what you do, your peers. They might be a level above you, a level below you. They might work at a bank or a merchant, but it's a very unique industry of people who want to find their tribe of people. It helps phone friends, people who are going to be there when you are like, “Man, I got hit by this fraud attack.” Usually they're always changing. Usually they have something you haven't thought of. To be able to lean on somebody who in turn then can lean on you, that's powerful.

Also, people who work in fraud prevention are really proud of the work they do because they can connect the dots to the real human impact that they're having. That was one of the thought processes, thinking a community might work really well for this industry.

Also, people who work in fraud prevention are really proud of the work they do because they can connect the dots to the real human impact that they're having. -PJ Rohall Share on XI'm going to be intentionally vague here, and I apologize for that. I know some people that they're not C-suite in their company. They report to the C-suite. They have good relationships with the people that report to the C-suite at their competitors.

They compare notes on a variety of things. “Hey, are you seeing this? Are you seeing this? I know we're not supposed to be talking because we're competitors. In terms of our job functionality, we're doing the same thing. Do you have any insights here that I can use?” It's interesting to see people share despite the competition and at the corporate level.

Yeah, especially on the banking merchant, I'll say the users of the technology. The vendors, it is a little bit different of a ball game. You're trying to scale your rules, machine learning, behavioral, biometric, identity verification, just fill-in-the-blank solution. You're less likely to probably collaborate at that level. But if you're working for a bank, you're working for a merchant, you're working for an insurance company, fraud happens in every industry.

It's a little different. Your bank wants to open up more accounts and sell more credit cards or whatever it is you do. The fraud teams, if they're not crushing you, they're going to be crushing them, and then they're going to be crushing somebody else. It's in the best interest to collaborate and share tips and tricks. It's not going to immediately, or I think even maybe ever affect how your company does versus the other company. We don't have the luxury of that.

If anything, we need to band together and collaborate more. Everyone's like, “Oh, we need to collaborate like fraudsters do. They're on telegram. They’re on the dark web. They don't have any rules. They don't also have many morals.” That's not realistic, but how can we do better? How can we incrementally do better? What our community and what Fraud Fight Club is getting people into person is to do better.

There are conferences, there are other communities, there are certification communities, and there are loads. We are taking our own unique approach to it. I say the more collaboration, the better. Getting the people there who are actually part of this fight and equipping, that's essentially our job. I'm an enabler in hopefully a good way.

I say the more collaboration, the better. Getting the people there who are actually part of this fight and equipping, that's essentially our job. -PJ Rohall Share on XI'm an enabler of relationships, being connected, of resources being connected. If you're working at one of these jobs full time, you don't really have all the time to network, research all these things, and go to maybe a million conferences. But if we can get you more connected and you don't have to find every fraud expert within your four walls of your company, then that's going to really help you upscale your career, but also just the value you are adding to the company that you're protecting.

Yeah. Before we get too much further into the conversation, I did want to ask you the question that I try to ask most of my counter scam, counter fraud, cybersecurity people. Have you been a victim of a scam or fraud, or someone close to you that you have a story to tell?

That's a great question. Fortunately enough, mine has been the vanilla version of fraud, which is credit card. You get your money back. A lot of the traditional unauthorized payment fraud activity where there's reimbursement and, God, thankfully not being manipulated psychologically or emotionally, like scams. I will say on a couple of points, anybody is vulnerable to this. I think breaking the stigma on this is one of the most important things to making some strides in scam awareness and having more people open up and tell their story.

I will say on a couple of points, anybody is vulnerable to this. I think breaking the stigma on this is one of the most important things to making some strides in scam awareness and having more people open up and tell their story.… Share on XIf you go through a scam, no matter whether you're vulnerable or not, you experience psychological trauma and shame because we look at scams as—even the word doesn't really amplify it enough. People's lives are being ruined. Some people's lives are being taken in the case of, just off the top of my head, sextortion scams. There's so much bad stuff going on. Vulnerable populations, elderly, even teens who are getting wrapped up in different types of scams. There's more vulnerable populations, but everybody.

I'm a 42-year-old, somewhat tech savvy, definitely fraud-savvy individual. We've had people like me or even more tech savvy who have come forward with stories of them being scammed. I remember allowing somebody to publish their scam story as a fraud expert, and that's powerful. It's powerful to see people who are not your prototypical scam victim telling their story. It normalizes it. It normalizes having a brain and human emotions.

Whether it wasn't a scam, but I can say I have been flooded by emotions. I mentioned OCD and anxiety. That's my particular thing that is tough for me. When I look at the decisions I make when flooded by emotions, urgency, and then look back on those, it can feel like it's not the same person making those versus a bit more level-headed, emotionally stable. I don't mean that in a stable versus super unstable.

When I look at the decisions I make when flooded by emotions, urgency, and then look back on those, it can feel like it's not the same person making those versus a bit more level-headed, emotionally stable. -PJ Rohall Share on XWe all go through stability and instability. I have two kids. If something's wrong with them, I'm trying to stay calm, but those emotions are flooded. I think we just need to be realistic about who the actual scam victims could be, which is everybody. We also need to be realistic about how it's being perpetrated these days versus 25 years ago when email was newer, and we were getting Nigerian prince scam emails, and we were like, “OK, haha. This is a silly thing no one would fall for. Maybe, maybe not, but it's nothing close to that anymore.

It's strategic, organized, in some cases, organized crime from overseas with big business models behind scamming that are putting so much effort into it to manipulate even the most savvy of individuals. It's a great question. I'm glad you asked that question actually.

It's interesting because most of the people that I've talked to, my guests who have shared about it, it's interesting because we are inundated with scams every day. In some sense, we're so inundated by that, we almost don't even notice it. I get that random, “Hey, I'm running late for the meeting” SMS message. “OK, it's a scam. You get that random phone call. There's so many weird things that we get that we dismiss because they're not contextually relevant to the moment in our lives.

There's a great story one of my guests was telling. He had bought something online that was being imported from another country. He knew it was coming from another country. He got an email saying, “Hey, there's a package for you that's held up in customs and we need you to do some paperwork.” It was like, OK, any other day, he wouldn’t have thought it was a scam, but because he was expecting a package, he started to do stuff, then got into it. “Why is my password manager not filling out the password?” It's like, “Oh, that's not the real site.”

When it's in context with something that we're doing, all of our spidey senses don't go off. The processes that we would normally go through don't trigger because it was exactly what we were expecting to happen in our life.

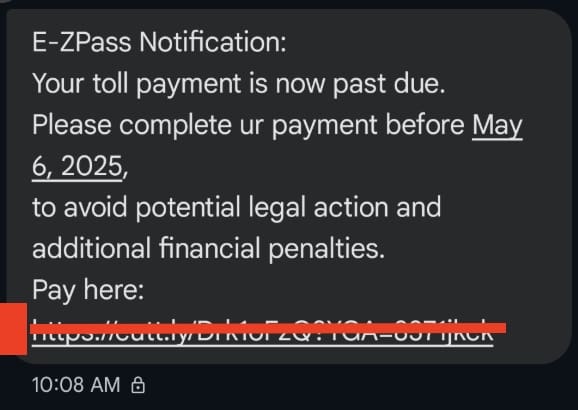

FAKE TOLL ROAD TEXT!

Yup, completely. I think the more we can look from outside of our own vantage point—I’ve gotten a million turnpike pole or toll things. We can all laugh about those things, but if someone's seen that for the first time, if they have something where it's like, “Shoot I might have gone through that toll,” then it's different.

I think with the blaming and the shaming, this is a larger probably societal issue where it's a lot easier for us to just explain how other people are stupid than look at, what is the problem? Do you think anybody was willingly like, “Oh, I can't wait to get scammed”? It doesn't need to be a personal level of responsibility.

There is a tricky balance there, but I think we get nowhere shaming and throwing folks under the bus. We get a lot of places by showing empathy in understanding and asking questions frankly about what they were doing at that time if we're trying to dissect ways to educate victims in the future. That's a whole ‘nother topic I know we might get into, so I'll stop there.

To me, that's the really interesting thing. I started the podcast about five years ago now, but even the mentality since then has really changed that there's a lot more empathy than there was five or 10 years ago towards people that have been a victim. There's a lot more understanding that this is not an intelligence issue. “They're just not a smart individual, so of course they're going to be taken advantage of.”

This is big organized crime, big business, and they're employing significant psychological practices into how they do what they do, and how they interact with people. If you and I aren't prepared for psychological warfare, how could we ever expect to get it right?

Yeah. We're in the industry of learning about this stuff, being exposed to it. It's part of the solutions in the market that are out there. It's part of the people I talk to, the teams they work on. They might not work in specifically scams, but we for better or worse are on high alert for people deceiving one another. What if you're not? What if you're just living your life and whatever level of technology acumen you have or whatever it is, and this is just something you come across?

My scam education dream is to get outside of our bubble. It's great to talk about inner bubble, because then you can educate family members, you can educate schools, you can educate wherever you can in your community. Getting outside of our bubble and getting on the loudest microphones with the farthest reach, and I mean them metaphorically or figuratively in the sense of streaming platforms, social media influencers, people who have wide reach and actual structured campaigns that have these PSAs that are way overdue.

We get emails from our bank. Great. To be fair, the bank's job is to educate you, but they're not sitting here. I don't want to say they're not creative. I want to say that they're a bank, so they educate their consumers just like they would like, “Hey, the APR of your credit card is going up, blah, blah, blah.” Some of them do some interesting things where they try to send emails and texts and say, “I will never ask for your one-time password.”

Could there be advancements in education? Sure. Could there be advancements in the way that they detect fraud? Absolutely. That's a different conversation, but I don't think it's on just the banks. I don’t. It shouldn't even come close to being on just the banks, especially from an education standpoint. From a societal—and then you break it out into country's government standpoint—what are we doing here? What kind of steps are we taking to inform our citizens of something that's well beyond financial fraud?

When it's financial fraud, it's devastating amounts of money. It's not hundreds of dollars, it's hundreds of thousands of dollars. The psychological trauma and that kind of suffering is the next level. -PJ Rohall Share on XWhen it's financial fraud, it's devastating amounts of money. It's not hundreds of dollars, it's hundreds of thousands of dollars. The psychological trauma and that kind of suffering is the next level. There are ideas I have and then there are ideas of what I think other groups can step up and do, but I think we're just so far behind the awareness and education curve that mainly takes advantage of people outside of our industry, even though people in our industry still obviously can fall victims of scams.

Yeah. There are two things that popped up in my mind in that conversation. The two-factor authentication messages have changed. It used to be, “Here's your two-factor authentication code,” and now it's, “Here's your two-factor authentication code. If you're talking with somebody, do not give this to them.” It's like, OK, the more that we see that, the more we're going to realize, “I should only ever be entering this in on a form, on a website, and I should never be giving these to somebody over the phone, particularly when it says, ‘Don't ever give this to someone over the phone.’”

Last year, I was in Singapore, and I was looking out the window of the hotel room, and there was an electronic billboard. Singapore is a very strong government in the sense of, “We have a lot of PSAs.” They want to do a lot of reinforcing, be nice, treat people well. There are ways that you need to behave in society, and the government's going to try to educate you and enforce that. There was this big electronic sign on the outside of a conference center that was, “If you get a phone call from a number that you don't know, stop. It could be a scam.” This was a PSA on a building.

On the rest of that trip, out at the shopping center was a little billboard saying, “If you see this, it's likely a scam. Don’t do that.” I was like, “Oh, wow. This country is taking the anti-scam into the streets.” It's not just, “Hey, I'm your bank. Don't give people your passcode.” It was, “As a government, we're going to try to educate you on the broad scopes of think twice before responding to these things.”

Definitely. That's great. Obviously every government's going to have their own way of how they want to enforce things for better or worse. I do think in the US, it's a bigger country, it's a lot more banks, it's a lot more citizens. There's got to be some type of cohesive overarching message in campaigns. Of course you can have different nonprofits and people tripping in. You see in other countries, again, maybe not at the scale of the US, not the size, but doing, I think it was in UAE, clever videos on YouTube and almost like a music video about not falling for scams.

In the UK, they have an organization called Take Five that does some things. Australia I think is on the forefront of I'm not sure it's just education, but how do we, from a regulatory standpoint, not just talk to the banks, talk to the social media companies, talk to the telecom. That's a big point of contention in the US. You have these scams happening upstream from the banks. I use banks, credit union, anywhere you can make a payment, basically.

There's really nothing incentivizing them to put in more scam controls, social media. I'm not going to throw any specific company under the bus, but social media, telecom as a bucket, there are more opportunities there. There are more opportunities to do stuff with the bank. But when you're a bank and pretty much everyone's going to where the thing ends and the liability ends, it is in the full picture.

Before that happens to anybody, the education and the awareness is such a big piece of it. Doing it from a government as opposed to just your bank sending something or a nonprofit being nice enough to jump in the fight, you might not want to learn everything in your life from educational things from sports, actors, or musicians. They have a platform, and people listen to them. They do all kinds of nonprofit work, why is something I call scamfluencers, which is a work in progress, why is that…

Trademarked.

Yeah, trademarked. Actually I've thought to myself as I've gone in many conversations about scams, I throw scamfluencers out there, and then the ego part of your mind is like, “Well, somebody could run off with that idea.” I'm like, “You know what? I hope somebody runs off with that idea.”

Please do.

And does something that is more meaningful. There are people who have platforms. I think part of the problem is that people who have these platforms don't know how bad it is. Everyone's going to have their causes. There's physical illnesses, there are other super-worthy things you would do PSAs for or raise money for, whatever it is. I think if some of these folks learned the magnitude of it, and unfortunately I think some of these more well-known folks will, whether it impacts them or loved ones they've had. I've seen Sandra Bullock reach out publicly about some scams. I don't think it was something that happened to her, but somebody was trying to manipulate her, her sister-in-law, or something along those lines.

This is much more pervasive in society than we think. It should be talked about no matter the medium, no matter the person. Frankly if you have a bigger outlet, then use that for good for scam education.

I think that comes back to the destigmatizing victims of scam and fraud. For so many years, people who've been victimized have been treated as, “Well, it was your fault. You shouldn't have done this. If you had just done this….” If someone comes up and randomly beats you up on the street, no one goes, “Well, it was your fault for the guy with the pipe hitting you.” Like, “I didn't instigate the fight; how is that my fault?” That's exactly how so many victims of scam and fraud get treated as well. It's their fault. Of course, people are not going to want to come forward under that environment.

Yeah. That's a great example. You could argue what if the person could have more, been a little safer in the physical? Maybe you go jogging through a neighborhood that's not the greatest neighborhood, you go jogging at night, or you do something like that. But if something bad happens to that person, I really hope and I'm pretty sure, no one's looking at that person saying, “You shouldn't have been there at that time.” Yeah, maybe there's some back channel scattered talk about, “Well, that wasn't the wisest choice, blah, blah, blah.”

The central theme is around the person who got attacked as a victim. The person who did the attacking, how do we make sure this doesn't happen again? How do we raise awareness? It isn't to say, “What an idiot; I wouldn't do that.” Therefore, let's just throw it to the side.

No one looks at a bank robbery and says, “Gosh, the bank just should have had four armed guards instead of three.” And then it would've been, “OK, gosh. If they didn't have all that money at the bank, they wouldn’t have been robbed.” No one blames the bank when the bank is robbed.

I think when you think about it, you mentioned the internet. I also remember when it came around. I was a little younger and doing the dial-up, that old awful noise, and AOL Instant Messenger when I was a teenager. It's new. Social media's really new in this scheme of life.

I think it's a bad convergence of a lot of things. All these things, even online shopping is, in the grand scheme of things, not all that old. You have all these ways to connect with people. You have all these ways to digitally get their money. You have all these ways to digitally manipulate them. We're catching up on a security standpoint, whether it's credit card fraud all the way to really bad scams.

With credit card fraud, it was the banks taking the liability and saying, “Hey, the losses come to me or the merchant.” There are different rules on that. It was like, “OK, citizens. Life goes on. Annoying. You have to get a new credit card shipped out to you. Life goes on.”

As you got more to faster payments, bank-to-bank transfers, Venmo, Zelle, and other countries, even earlier, the UK was 10 years, 15 years ahead, of us with faster payments, not surprisingly, they felt the brunt of scams sooner because it was like, “Wait, I can tell this person to send this amount of money to my bank account, and I can immediately take it out.” That's wow. That's what frauds in general do. They look for areas of opportunity. They look if there's a good ROI and they pounce on it. They're business people at heart, the bad good ones, but the good ones.

All of this is relatively new. There's also this problem of it going across industry. You have one company where it starts, goes to a different industry, another company, and it's like, “Who owns this? Who owns this problem?” The government's like, “Wait, what? This is that bad of a problem?” Not to mention if you've lived in any country, there are a million other problems going on too. How does this get to the front-and-center news issue?

I think that is a challenge. That's also where I think more prominent people speaking about it will get media attention. It just does. When I say something, ABC News is not ready to interview me. I don't think so, at least. When somebody else says something, Taylor Swift makes a tweet, it is top of news.

Yeah. OK, Taylor. All the Swifties need to ask Taylor to talk about scam prevention.

There you go.

Get in touch with either of us. We'll be happy to give you talking points.

Or Ryan Reynolds. For some reason, Ryan Reynolds always comes in my head as a quirky guy that would go out there. I think it's because he has Mint Mobile commercials and he knows. He does things like the soccer team with that other guy. If anyone knows Ryan Reynolds, just contact me.

We'd be happy to facilitate a discussion on a campaign.

I'm a completely normal person.

Are there other approaches we should be doing differently than what we have been doing? Clearly, I think getting influencers on their soapboxes, talking about it and explaining it, and trying to destigmatize it is massive. What are some of the other things that we can do differently?

Yeah, a bit more traditional and also downstream. Once this stuff gets to the banks or the FIs—I remember working in merchant fraud and when there was a problem, whether it was a customer calling in or a person pretending to be the customer who was a fraudster, I get on the phone and say, “Let me resolve your issue. Sorry, we canceled it for fraud; let me get it reprocessed.” That was—uncomfortable conversations.

I ruined too many kids' Christmases probably by canceling their orders for fraud. My bad. Hopefully I didn't really ruin anyone's Christmas. Basically, they got their item. It just was like a day or two later. I don't want anyone thinking I ruined Christmases.

Those conversations, I remember, made me super anxious. Imagine that, but you're at a bank and somebody calls up and says, “I've lost $200,000 to a scam. What do I do?” I am in a state of panic, anxiety, and probably, eventually depression or some type of psychological and emotional states that people who are working on the phones handling fraud and scam cases are really not equipped to handle. This is all to say I think, and I've seen a little bit of a trend of this, hiring and employing actual psychologists, people who understand human behavior to revamp that whole journey, that customer journey, not how they're going to buy a banking product, but if a scam might be occurring, has occurred, the victim's calling in, wherever it is in that journey, how can we design this process from a standpoint of understanding that person's psychological state?

If it's too late and we need to support them from what are the next steps with an empathetic lens that people need to be trained in, OK, how can we do things upstream in the banking journey, digital or in-person, where we can ask questions and be inquisitive about why they want to send $35,000 to an account they've never sent before overseas? It's a really delicate conversation.

There are people who have studied psychologists, not me, who would have advice that it might be counterintuitive to what you think because what you want to say is, “This is fraud. This is a scam. Why would you do that?” That cannot be the best approach. There can be other ways to interact with the customer to design products with that in mind, to design warning messages. OK, I'm about to make a transfer. I see this in Zelle. It's like, “This is a new recipient. Beware of scams.” Those are great steps.

That's not easy. Those are things that take, if it's designing a whole product journey, that's product teams. That's months of planning and years maybe in the roadmap to get to roll out that product. You can't probably, realistically, if you're a financial institution, hire armies of PhD psychologists. That's not affordable, nor it's just not a feasible thing.

I don't think they would mind me saying this, but there's a great person, Elizabeth Huppert, and I probably butchered her last name, who works for JP Morgan Chase on their scams team and was hired for just that reason. She came to Fraud Fight Club, our conference, to provide a different perspective. She is a smart PhD student graduate with a really strong understanding of behavioral science and psychology. They can chase something that a banker or a fraud fighter can't. It was a very forward-thinking move of them to bring someone like that in. I know other banks and financial institutions are thinking of things like that.

I think thinking differently than what we've traditionally done is one thing. These type of psychologists are one example of that. Also, there's more and more technology on the market that is designed for, specifically scams. I think there used to be ones that were very fraud focused, basically unauthorized. It's a different thing than when it's the authorized person. The customer is saying, “Hey, I want to make this payment.”

Banks, merchants, or any company that is willing to invest money and budget into procuring technology to help protect their customers is what we should be doing. That can be a confusing journey to get budget. “Wait a minute. Do we have any losses?” “No.” “Then we're not spending money on it.” That can sound very heartless. What do you mean?

I can't make those decisions for companies, but I do think we are reaching an inflection point, where your customers are going to look at institutions to prioritize their wellbeing from a scam perspective. If they see others leading the charge in that, they're going to say, “I'm not going to bank here, I'm going to bank here. I'm not going to buy my product on this marketplace, I'm going to buy here.” How soon that happens and how you fit that in your business case, I'm not sure. I think more forward-thinking institutions are putting aside budget to maybe hire a psychologist, to maybe institute a scam tech tool that is more new or cutting edge, whatever that means, and are not strictly looking at, “Did we lose money where we are accountable for?” That's one lens.

Maybe in the USA, in the UK, there's liability for banks in certain cases and a lot more cases in the US. The government right now is not looking like anytime soon it's going to impose regulations that say the banks are liable, but that doesn't mean that's the only reason you should get technology or resources and think differently. There's loads of other reasons that you could be at the forefront.

You can spin that conversation to be this is a customer experience of revenue-generating exercise. This isn't a cost savings. You can be at the forefront of a crowded field of businesses that are not talking about scams at their forefront. Heck, bank, you can be the one that contracts with Ryan Reynolds to bring you on as the person who's leading that. I'll even let you steal that idea. Anyway, those are my thoughts.

Yeah. You're at a disadvantage if you're a major financial institution if you're waiting for the government to require you to change. You really don't want to be in that position where the government says, “OK, you now have 30, 60, 93 years to hit this goalpost.” You better be working towards that goalpost before they tell you that you need to work towards it.

Absolutely. That was a succinct way of summing up some of the things I said. Thank you.

It's easy because I heard you communicate it. If people want to learn more about what you guys do, where can they find you online?

Yeah, I'm on LinkedIn potentially a little too much. I don't dive in any other social media other than that, and I try to keep it somewhat interesting. My personal LinkedIn, always feel free to reach out, About Fraud. Our website, about-fraud.com. There is a dash in there, but honestly, if you just google us, you can find us.

Fraud Fight Club. Fraud Fight Club is our conference. We like to call it a club, not a conference. If you want to actually understand what it is, it's not someone's basement where we're beating the crap out of each other. It is a club. It's more of a community of like-minded individuals who professionally work in fraud prevention and want to connect with other people who have that passion and have that interest. Fraud Fight Club has a website, has a LinkedIn presence. You can email me at pj@about-fraud.com. I would imagine if you have any digital savviness, it won't be hard to find me.

We'll make sure to link to the about-fraud.com. We'll link to the right one in the show notes.

There you go.

PJ, thank you so much for coming on the podcast today.

Yeah, thank you so much for having me and giving me some time to air my thoughts. Thank you.

Thank you.