The burden is on consumers to question the validity of online offers because privacy laws and standards are not yet well regulated. Consumer Reports is fighting to make changes in this arena. Today’s guest is Marta Tellado. Marta is President and CEO of Consumer Reports, the independent non-profit that works side by side with consumers to create a fair and just marketplace. She is a market driven leader with a passion for innovation, public-service, philanthropy, and helping organizations maximize and improve the world.

“When you’re going to the marketplace, most of us assume that what is there is safe and not harmful so we go about our shopping. The reality is, unfortunately, it is not as safe as we would like to assume.” - Marta Tellado Share on XShow Notes:

- [0:55] – Marta shares her background and her role as CEO of Consumer Reports.

- [2:19] – We’re at a pioneering moment in the consumer market. Regulation hasn’t transitioned into the digital marketplace.

- [4:04] – When online, we assume everything we do is safe.

- [5:52] – Now with AI, consumer awareness is even more important.

- [7:41] – As technology advances, so does the potential for scams.

- [9:27] – Be aware of the red flags.

- [11:33] – Consumer Reports has a ton of resources and information on scam protection.

- [13:17] – Everyone is a target and anyone can fall for a scam, including Marta.

- [15:51] – Marta shares the estimated amount of money lost to scams in 2022 and the increase we are seeing.

- [17:45] – Instead of connecting your peer-to-peer payment accounts to your bank account, connect them to your credit card where you have more protection.

- [20:17] – Even when we select the “unsubscribe” button, we may be flagged as someone who is interacting with the scam content and further targeted.

- [22:58] – The rules and regulations aren’t keeping up with the rapid growth and development of technology.

- [24:55] – Marta describes the ways Consumer Reports works to educate consumers.

- [26:25] – It takes a really long time to get laws and regulations in place.

- [29:01] – We can’t see or feel the things that keep us safe or harm us online.

- [31:38] – Even if you feel that you don’t have anything that a scammer would want, be aware that any information is valuable to them.

Thanks for joining us on Easy Prey. Be sure to subscribe to our podcast on iTunes and leave a nice review.

Links and Resources:

- Podcast Web Page

- Facebook Page

- whatismyipaddress.com

- Easy Prey on Instagram

- Easy Prey on Twitter

- Easy Prey on LinkedIn

- Easy Prey on YouTube

- Easy Prey on Pinterest

- Consumer Reports Home Page

Transcript:

Marta, thank you so much for coming on the Easy Prey Podcast today.

It’s great to be here, Chris.

Can you give myself and the listeners a little background about who you are and what you do?

I am the CEO of Consumer Reports, and it has been an honor to be leading this iconic organization that has been around for 87 years. It’s an organization that is trusted by so many consumers in the marketplace, but we’ve had to earn that trust over the years.

I would say that primarily it’s because we’re very independent, we’re nonprofit, we’re completely supported by our members, and unlike a lot of some of those review sites you might stumble into out there, we don’t take any advertising. We’re not beholden to anyone or any advertisers.

In light of what’s going on in the marketplace and what you focus on is scams and fraudsters, it seems like we’re more relevant than ever. We have a job to do by investigating, educating, and advocating for consumers. I’m really looking forward to talking about some of that with you.

Awesome. What is the mission statement for Consumer Reports?

We work hard to create a fair and safe marketplace for all consumers. What we do is we show up when the marketplace fails and when the government fails to protect consumers. We try to create standards where none exists. We’ve been around for 87 years, so we’re pretty proud of some of the things we’ve been able to do.

But as we have pivoted to a digital marketplace, a lot of those rules, regulations, and protections have not migrated into that space. We’re at a pioneering moment for consumer protection. When we look at the consumer power, that has really waned as we have migrated over to platforms and social media, and you have to really watch out for those scams.

Let’s talk about that. Were you guys surprised by the speed at which things have transitioned from the physical world to the digital world?

It’s been a pretty steady stream. We have been on the Internet for a long time now. I think it started with Amazon and books, and now we’ve gone from bricks-and-mortar shops to shopping malls to platforms.

Now, the buying experience is not only just a transaction to buy something. You’re offered financing, you’re offered a whole way of payments as well. I think the whole shopping experience has changed, and it feels like in the last several years that change has really accelerated.

And even the concept of physical goods is transitioning away now. We have so many digital goods in one respect or another as well.

Yeah. We’ve also gone from a cash economy to things like peer-to-peer payment apps. What we’ve learned in our 87 years is that when you go into the marketplace, most of us assume that what’s there is safe and not harmful, so we go about our shopping.

The reality is, unfortunately, it’s not as safe as we would like to assume. So we try to partner with consumers to keep our searchlight out there. What needs to be strengthened for consumers in all aspects of the shopping platforms?

What are some of the major assumptions that consumers are mistakenly applying to their online experience?

The online experience is not like when you look somebody in the eye, you go cozy up to the cash register, and you pay for something. And then the person next to you buys the identical object and pays for it. You both pay the same thing and you both witnessed it.

On the online marketplace, I may dial up to get plane tickets, and based on what that platform knows about me, my zip code, my income, they might charge me a little more than they charge the next person. So how do you police that? Is that fair? We don’t think so. But it is also quite legal. We don’t really have any rules and regulations that can tame what they call dynamic pricing.

And now with AI, think about that as you create chats about a product, about the marketplace. That algorithm is scraping the Internet for answers. It’s not necessarily verifiable, so again, we really have come to depend on technology.

Technology in so many ways has made and transformed our life in some wonderful ways, but it’s really way ahead of the consumer regulations, protections, and standards that we need. It’s just racing way ahead of what we can get our… Share on XTechnology in so many ways has made and transformed our life in some wonderful ways, but it’s really way ahead of the consumer regulations, protections, and standards that we need. It’s just racing way ahead of what we can get our arms and legs around. I think consumer awareness is now so much more important than it ever has been.

There are multiple facets to this AI surge that we’re having. You’ve got the content building from it, using AI as a research tool.

There was a great story a while back of a lawyer who, in my impression, I should say because I’m not a lawyer, shortcutted the process, couldn’t find the arguments that he wanted for his case, so he went onto his favorite AI engine and said, “Find me support for this legal position.” So it generated this. “OK, provide all the case notes and everything for it.” So it provided the case notes.

He went to court and the other side was like, “None of those cases actually exist.” That’s one of the challenges with AI. It’s confident, but it can be confidently wrong. I think they call it hallucinate facts when they’re not in existence.

Yes, it’s hallucinating with confidence, as you say. Just put the information out there. But I think the punchline is with generative AI. As technology advances, so do the potential for scams. As I said, it’s hard to keep up at the pace of technology.

Take AI and the rise of voice cloning. People used to think, “If I get a call from someone and I recognize their voice, then it’s not a scam.” But in fact, you could take snippets of somebody’s voice, either from a phone call or from an internet engagement, and you can clone a conversation. And that has in fact happened.

We’ve had a lot of victims of voice cloning, where somebody gets on the phone with you and tells you someone you know is in distress, and it’s quite believable. It sounds very authentic. That’s yet another way in which technology has created more opportunities for scamming and fraudsters take advantage of the technology.

That one is particularly concerning to me. I’ve heard so many stories about parents getting a phone call from what sounds like their daughter. “Help me, help me. I’ve been kidnapped. I was able to grab my phone.” And then the would-be kidnappers get on the phone and the standard ransom story.

Any good parent in the moment is going to be like, “Don’t care about the money. I just want to keep my kids safe.” That becomes their top priority, and the scammers, unfortunately, just benefit immensely from these things.

The thing to keep in mind is be conscious of what the red flags of fraud look and feel like. Let’s face it. The frauds and scams have existed for as long as the marketplace has. They always prey on your emotions, and they always… Share on XThe thing to keep in mind is be conscious of what the red flags of fraud look and feel like. Let’s face it. The frauds and scams have existed for as long as the marketplace has. They always prey on your emotions, and they always have a good story to tell.

It’s either something joyful—you’ve won something—something you should be afraid of, or, “Hey, look. Someone’s in need. Help them.” Those are the emotions and the heartstrings they pull on you now. But don’t fall for that promise that you just won something.

I’m sure this has happened to you. You go online, you’re shopping, and you get this pop-up note that says, “You’ve got to act now because this deal is going to change in 30 seconds.” Don’t buy it. It’s a tactic. And don’t buy the you-have-to-pay-upfront one either. Those red flags.

I got a call the other day from my bank. It happened to be a legitimate call. The first thing I did was I asked the gentleman for his name, and as he was giving me his name, I was googling. I was saying, “Is this guy real? What’s his name?” He was very forthcoming, it turned out to be.

But you also don’t want to just believe something on the phone. You want some written information to come to you. Don’t be scared into doing anything or buying anything. There are all kinds of ways to even raise your awareness even further.

That’s why we devoted a whole issue in July to protecting yourself. What are the best tips, the smartest tips, for you to think about this whole new world of digital fraud and scams.

I know the magazine that you guys sent out is specifically to your paid members. Do you have a digital version of that that’s available to the general public?

We sure do. We have actually many more digital visitors; millions come to our site every day. We’ve got a lot of stuff for everybody who comes. All you need to do is come to cr.org, look up the Scam Protection Guide, and it’ll come right up. It gives you the best tips, what to do.

When you think about scams, it’s about how to prevent money from being taken out of your bank accounts, how to have your personal information stolen and tracked, and your personal identity, your Social Security number, ways in which you can get scammed. So all the different ways that you could strengthen your own personal security.

It’s unfortunate that the burden is on consumers right now. That’s the reality. What we can do as an organization that is really all about consumer power is we can fight on behalf and with consumers for those standards, those protections, and how to strengthen those rules of the road, so that a lot of what we have experienced in the physical world, we can start to see those protections in the digital world.

Let’s talk about that in a minute. The premise of the podcast is really helping to prevent people from being scammed. Part of that is getting people to be able to talk about it, the realization that it does happen to way more of us than we think it does, and trying to de-stigmatize that. Have you or anyone that you’ve known become a victim of a scam?

Oh, yes, absolutely. I think of my own personal story, like how did I even come to this? Like, why is Marta Tellado, the CEO of Consumer Reports, so rabid about consumer rights and preventing scams?

My story is similar to many, but with a certain twist. A lot of us came to this country as either immigrants or refugees, as my family did. We moved here from Cuba and there was a lot of appreciation for coming to a country that was open, fair, free, and had a variety of opportunities. They weren’t guaranteed, but if you understood the rules of the road.

As a child, you begin to advocate for your parents because you pick up the language a lot faster. I got pretty good at translating what I was saying, of course, in way over my head. But if you think about it, all of us at one point in our lives, go into the marketplace because that’s where we fill our aspirations. Whether it’s a car loan, car insurance, a mortgage. And it’s really hard to navigate that.

I decided I want to serve. I want to give back. I want to be able to make sure that everyone has an opportunity at success and they’re treated fairly in the marketplace. But what happens when you don’t?

Here’s an example that really has to do with my dad. So many of us think scams only happen to the elderly. This happens to be an example where that’s the case, but you’ll see that it could happen to anyone.

He’s been a type 2 diabetic for most of his life, got on the Internet, and he got tracked because he did not have any of the safety stuff that I’ve since piled into his devices. He started getting pop-up ads selling him that the drugs he was on were not effective. This was all this person in a white suit looked like a doctor. Guess what? He stopped taking his medication, he didn’t tell anyone, and he started to spiral.

I finally was able to get it out of him. When you’re taken advantage of, your instinct is to be embarrassed and to hide from it. That’s the wrong instinct. These are criminals, these are fraudsters. A lot of times, you really do need to call them out and you need to file a police complaint as well.

That’s a serious example. There are many where people have seen their life savings taken away. I’ll just give you one statistic. $8.8 billion is believed to have been lost to scams in 2022. That’s twice as many as 2020. We are seeing an acceleration in the digital world.

$8.8 billion is believed to have been lost to scams in 2022. That’s twice as many as 2020. We are seeing an acceleration in the digital world. -Marta Tellado Share on XThat’s crazy. You’re talking about Consumer Reports fighting for standards. What are some of those standards that you’re fighting for that may help lead to a reduction in this online crime?

One of the things we don’t have are real privacy laws. We’re pretty fair game. If you’re on the Internet, and you’re unsuspecting, and you’re filling out all the forms, and you’re even taking these pop quizzes that say, “See how much you know about X,” these are all marketing schemes. Marketing geniuses that know how to get your attention, know how to get you to engage, and to give up information about yourself.

We don’t have a federal privacy law that actually allows us to delete our information. It allows us to own the information we have, to have people and marketers stop tracking and selling our data to third parties.

We have a couple of states out there that have done a really good job, so we’re hoping that by working on the ground with consumers, we can start to see some of this take root. We’re also fighting for things like peer-to-peer payment apps, for example, that are not really protected by a lot of the banking laws.

You probably all use something like Zelle or Venmo. If you make a mistake on Zelle and you just happen to get the wrong phone number of somebody, and that money’s gone, it is gone. There’s no obligation for them to make you whole.

One good tip to know—I’ll just throw this out for your listeners—is instead of connecting your peer-to-peer payment app to your bank account, connect it to your credit card where you actually have more protections there. We’re working with some of the regulatory agencies to make sure that happens.

Instead of connecting your peer-to-peer payment app to your bank account, connect it to your credit card where you actually have more protections there. -Marta Tellado Share on XWe’re also really fighting for some real penalties and fines that make a difference. These are huge billion-dollar platforms. Sometimes a fine is just the cost of doing business. It’s not really paying for them. That’s got to change as well.

Are you thinking about laws more towards Europe's GDPR style on privacy?

They’re way ahead of us on thinking about how to protect consumers. I’d love to see some of that in our culture where we think about what our privacy is worth to us, what our security is worth to us, cyber crimes. Think about that. We know that the technology is out there to be able to do that, so we’re iterating with new tools as well.

We are putting out in the market soon something called Permission Slip that is actually going to serve as a private consumer agent to anyone who’s got this app. It’ll be available on the App Store, and you’ll be able to control who you want to block and let in and share your information with. But again, right now the burden is on consumers. We need to get the burden placed elsewhere. It’s too much to keep track of.

It’s definitely a challenge, and I think you’re talking about marketers. Companies have—maybe really good is not the right phrase I want to be using—been skilled at acquiring information from us in ways that seem to benefit us. “Give us your birthday and we’ll send you a $5 off coupon for something. Give us your email address and we could put you on our mailing list for discounts. Give us this and give us that.” In the moment, we think we’re getting something great for, but I always think of like, if they’re willing to pay me $5 for something, that means they’re sure that they’re going to make at least $5 in profit off of me because of this.

That’s right. And Chris, I’ll tell you another thing. Many of us think, “Oh, I’m going to not press that button that says unsubscribe.” What we don’t realize is sometimes when we do that, they’re like, “Oh, I got a live one. There’s somebody really there. They’re responding, they’re engaging.” So you can’t even trust that sometimes.

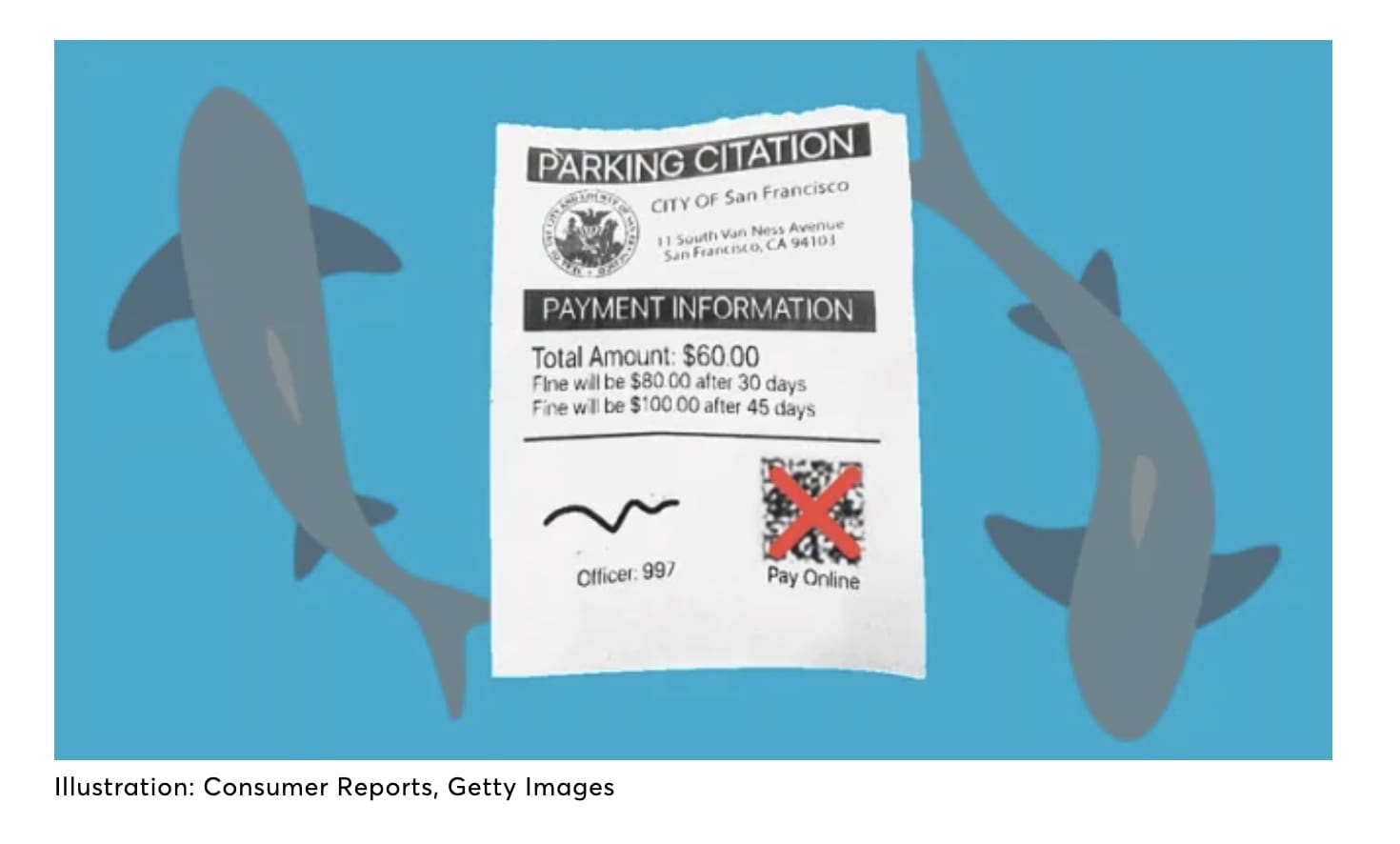

The other piece that I’ve learned about recently is QR codes. We use it a lot. We had a program called CR Recommended, where you actually are in-store or online, you see a product and you see our logo recommended, and also, if you’re in-store, can do a QR code. I’ve also seen where you’re at an event, you get to your car, and there’s a flier on your car with a QR code that says, “You’ve just been ticketed. You need to press this QR.” It’s a scam.

You just have to have that awareness and cast a side eye until we can really impress upon regulators and businesses that putting consumers first is a good thing for your brand.

Awhile back, one of the neighborhood kids was fundraising for something or other. They went around the neighborhood and put a little flier with a QR code on everyone’s door. It was like, “Hey, can you help me out?” And there was a QR code, no explanation of what it was. I’m like, “No, I’m not going to be scanning that.”

That’s right.

It’s one of those things so many people…”Well, what could be the harm of doing this?” But I think the ones you talk about, like the parking tickets, are a great example. I’ve heard of them doing the same sort of thing with parking meters. “Oh, you can pay for your parking by just scanning this QR code.” It goes to my fake parking location dot info and you pay your $5. You think you’ve paid for your parking, but you get a ticket and they get $5 out of you.

That’s right. To your question on what else we could do—this isn’t the first time we’ve been here. There was that incredible moment that some of us will remember: ATMs. Nobody goes to a bank anymore. They go to an ATM. Well, there were all kinds of problems there when that new technology came out. We figured it out.

That’s why there’s a thing called the Electronic Funds Transfer Act. We want to make sure that peer-to-peer payment users are included and that fraud protection. Again, the rules and the protections for consumers aren’t keeping up with all this great technology.

That technology can also be used to enhance the buying experience in ways that are protected and secure. That’s what we’d love to see and that’s what we’re going to continue working on.

And that’s always the balance. Went to dinner with friends the other night, and the waiter didn’t want to split the check. So it was like, “OK, will everybody give me cash or do a funds transfer to me? And I’ll pay the bill on my credit card and a little bit of cash?” One person decided to use Venmo. There is definitely that advantage of it’s as good as cash. It’s quick. But the challenge is, if you make a mistake or if you were scammed into doing it, now it’s gone.

And it comes down to consumers. We have to demand those kinds of changes. As I said, technology is racing forward, but we’ve seen how you can put protections in place and it does not get in the way of innovation. These two things are not mutually exclusive. We have to say this is what we’d like to see in the marketplace.

Is some of the advantage of Consumer Reports’ role in that is that you do have a bully pulpit in the way that maybe individuals or smaller organizations don’t?

I think we have a number of tools that we use really effectively with consumers. There are some things that we were able to investigate, and we see that in some of the safety pieces that we’ve done. We just got done testing the safety of water that comes out of your tap and the PFAS chemicals, and we’ve been able to train volunteers across the country to test their tap water.

It’s a way of bringing evidence and engaging people to have some agency and the change they want to seek. And then of course, it’s the labs. We have 60 labs. We have an auto test center that tests all the cars. We buy all the products that we test. As I said, we don’t accept any advertising, so you’ve got to have that trust.

We’ve got so much information at our fingertips right now, and what we’re lacking is that trust and that guidance. Like, “Who can I trust?” There are also a lot of fake reviews out there, so we try to give you tips on how do you spot one? What should you be looking for? How do you make a decision? Especially on those big ticket items where you really have a lot at stake.

We try to combine the investigations, the ratings and reviews, as well as all the testing that we do to create a real powerful voice for consumers in the marketplace. These companies, we’ve seen more and more concentration in the market. Their power is outsized relative to what a consumer can press upon them.

These are companies that are selling things on the market. Consumers, it’s supply and demand. We need to demand some things. I’ll give you one very vivid example of how you can actually move a marketplace.

What we know is that sometimes it takes a really long time to get standards and laws in place. In the interim, consumers are suffering, especially when safety’s in mind. When you look at cars, we are so proud that we were championing seatbelts before they were law, and now we just take it for granted. That was the technology we had.

We all know that there is amazing technology in every vehicle right now—blind spot warning, pedestrian lane changing—and we have enough research to know it’s life saving. But some of that stuff is still a luxury. So what does that mean? Your safety and the lives of your family is an add-on luxury as opposed to something that’s demand? What we said to the manufacturers is, “If you don’t have these lifesaving technology standards, we’re not going to put you in the top 10 category.”

Suddenly, you start to see movement. They want consumers to know that they’re going to be safe in their cars. That’s another way where, working en masse, we could see markets change. We could see that safety. That’s what we’re hoping is going to happen around all these digital tools. We’ve got to raise up our consumer voice and say we actually want a digital world we could trust.

I remember growing up my dad’s car, which is the oldest car that we had in the family, had no seatbelts in the back. And the front only had the lap belts. There were no shoulder belts. It’s so interesting to see how over the years, it really is now seatbelts—front, back, shoulder harnesses, pretensioners, all the amazing stuff going on.

What you’re saying, those are all things you can see, feel, touch. In the digital world, you can’t see or feel what’s protecting your cash. You can’t see or feel what’s protecting your personal identity. That’s why we have the Scam Protection Guide, and we also have something else called the Security Planner. You could also get that at cr.org.

What that does is you can just go to the Security Planner, go through all of your connected devices, and maximize them for security and data scrubbing. I just invite your listeners to run through the drill. Just takes a minute. Yes, the burden is still on us, but I don’t want you to be out there and unprotected in the interim while we’re fighting for consumer rights and privacy in that marketplace.

In my personal life when I’m talking with my friends and stuff, I’m always an advocate of always ask a company why they want something from you. If you’re buying a pizza and they want your birthdate, “Why do I need to give you my birthdate in order to buy a pizza from you online?” That doesn’t seem reasonable.

I’ve even done this a little bit at the doctor’s office. “What’s the reason you need this data? Can I still have my appointment without providing you this information?” And just trying to be in a mindset of, “I’m only going to give what is required in order to get the service that I need.”

Chris, that’s a big step. You are actually challenging someone in a completely reasonable way. I think consumers need to feel comfortable doing that, even in the doctor’s office when you get asked.

All of us text a bazillion times a day. We do. Either talking to our husband, talking to your kids, you’re all texting. We have seen scams really take off in texting as well. Avoid clicking on those links. Just don’t go. Do you know this person? Think about what you’re conveying in those text messages.

We used to worry about those robocalls. Still do, and there are still some great software that can get to screen those. You’ll screen out the sales pitches. You might not screen out all the fraudsters. So it’s not foolproof.

Wait, you mean the scammers don’t always play by the rules? That’s the unfortunate thing. Like the federal Do Not Call list. Ethical businesses, if you’re on that list, aren’t going to call you. But unethical ones, they’re still going to continue to call you.

That’s right.

As we start to wrap up here, do you have some tips that would be good for consumers to just reduce their chance of being scammed? Things that should be red flags they should be watching for, or just good practices?

I thought we talked about some of those red flags, so I would double-down on those. Remember, these scammers and fraudsters are going to play on your heartstrings. You’ve got some pretty valuable things that they want—your personal identity, the money that they could transfer digitally quite easily these days, personal information that they’re going to sell to third-party data folks, and hacking.

If you are a victim of hacking, the first thing to do is freeze your credit. Call Equifax, Experian, TransUnion, and let them know. That happens so much and so often, and unfortunately, many companies do not notify consumers and victims of hacking in a timely fashion. We’ve seen that time and time again, so you need to get a jump on it when it does happen. You’ll see some guides for that as well on cr.org.

You’re going to have to take matters into your own hands for the time being. Make sure your devices are secured, you have optimal privacy, scanning, and minimal amount of tracking on your devices. Go to that Security Planner on cr.org. And also, the Seven Smart Security Steps in our Scam Protection Guide. I think those are a great place to start. Think about other ways in which you want to be part of a consumer community that’s really trying to shape the community to put people first.

I love it. We’ll make sure that in the show notes, we link to the Scam Protection Guide and the Security Planner. Make it easy for people to find. But you can also go to cr.org and search for them in the nav bar. It’ll pop them up. I found them quite easy doing that. I appreciate it when people who build websites make it easy to find the tools that we talk about.

Thank you, Chris, and thank you for what you do by devoting so much time and attention to an issue that’s often in the shadows. We do want to trust. Unfortunately, there is a rapidly changing digital marketplace out there that is not as trustworthy as many of us assume. I hope that Consumer Reports along with consumers can work together to change that.

Absolutely. Thank you so much for coming on the Easy Prey Podcast today.

Thank you, Chris. A pleasure to be here.