Fraud doesn’t always announce itself with obvious warning signs. Quite often, it shows up wrapped inside something that feels routine — a purchase you’ve made before, a link that looks legitimate, a message that arrives at just the wrong moment. Nothing feels suspicious, so your guard stays down. By the time questions start forming, the transaction is already done.

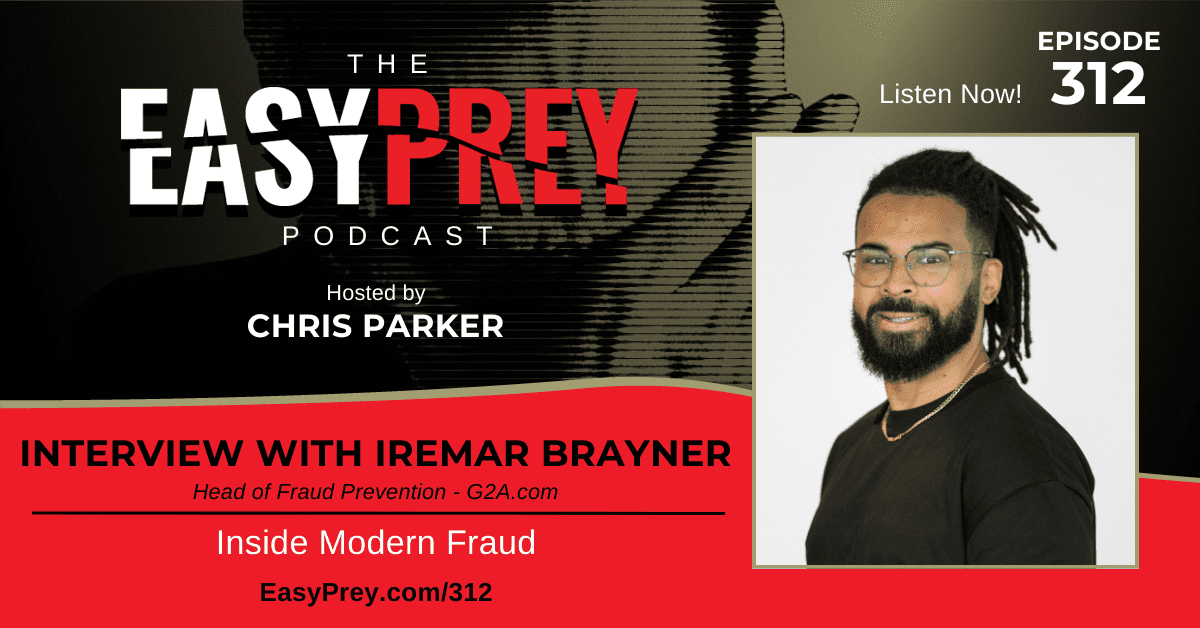

My guest today is Iremar Brayner. He’s spent more than 15 years working in fraud prevention and risk management across payments, retail, ride-hailing, fintech, and digital marketplaces. In his role at G2A, he leads fraud strategy for one of the world’s largest digital entertainment platforms, where speed, approval rates, and loss prevention are constantly pulling against each other.

We discuss why scams continue to work despite smarter tools, how “friendly fraud” complicates the picture, and why digital goods create very different risk patterns than traditional retail. We also get into automation, AI-driven decisions, and what it really looks like to manage fraud in real time.

“Friendly fraud is one of the most complicated challenges we face because the customer actually received the product.” - Iremar Brayner Share on XShow Notes:

- [1:36] Iremar shares how his career in fraud prevention began, moving from bank customer service into reviewing suspicious transactions.

- [2:45] He explains why he completed law school but chose not to become a lawyer, and how legal training shaped his understanding of fraud psychology.

- [4:10] Fraud is framed as an emotional event, with urgency, financial stress, and excitement often lowering a person’s defenses.

- [6:16] Digital marketplaces attract fraudsters due to low-cost items and products like gift cards that are easy to cash out.

- [7:10] The concept of card testing emerges, where stolen payment details are validated through small purchases.

- [8:05] Iremar discusses the rise of friendly fraud, where legitimate customers dispute transactions after receiving goods.

- [9:30] Major product launches, such as highly anticipated game releases, create predictable spikes in fraud risk.

- [11:05] Marketplace fraud requires managing risk on both sides, verifying sellers while monitoring buyers in real time.

- [12:40] He describes G2A’s shift away from manual review toward fully automated transaction decisioning.

- [14:15] The tension between frictionless customer experience and effective fraud prevention is unpacked.

- [16:05] Automation and AI are positioned as essential tools for scaling fraud defenses without overwhelming operations.

- [18:10] AI’s real impact is discussed: not changing fraud itself, but making attacks faster and more scalable.

- [20:05] Iremar explains why human judgment still plays a critical role alongside AI systems.

- [21:41] Fraud patterns differ across industries, illustrated through examples from ride-hailing platforms.

- [23:10] Abuse of referral and incentive programs reveals how self-referrals became a common fraud tactic.

- [24:40] Identity misuse by drivers highlights risks tied to document verification.

- [25:50] Face recognition and customer reporting become tools for detecting account misuse.

- [27:15] High-value luxury marketplaces introduce entirely different fraud and logistics challenges.

- [29:10] Practical consumer advice: buy from reliable sources, review refund policies, and question unrealistic pricing.

- [30:05] Seller protection strategies focus on accurate product descriptions and shipment tracking.

- [32:05] The most common complaints in marketplaces are items not received and items not as described.

- [33:20] Iremar recounts becoming a fraud victim after a fraudulent airline ticket charge.

- [35:00] A WhatsApp impersonation attempt using his photo targeted his mother.

- [36:10] Verification habits are emphasized as one of the strongest defenses against scams.

- [37:40] The risks of social media and account takeover scenarios are discussed.

- [39:30] Challenges around encouraging broader adoption of two-factor authentication.

- [40:05] Career advice for those interested in fraud prevention as a profession.

Thanks for joining us on Easy Prey. Be sure to subscribe to our podcast on iTunes and leave a nice review.

Links and Resources:

- Podcast Web Page

- Facebook Page

- whatismyipaddress.com

- Easy Prey on Instagram

- Easy Prey on Twitter

- Easy Prey on LinkedIn

- Easy Prey on YouTube

- Easy Prey on Pinterest

- Iremar Brayner – LinkedIn

- G2A

Transcript:

Iremar, thank you so much for coming on the podcast today.

Thanks for having me, Chris. Really happy to be here.

Awesome. Can you give the audience and myself a little bit of background about who you are and what you do?

Yeah. My name is Iremar Brayner. I'm originally a Brazilian, but now I'm living in Portugal. I'm a fraud prevention and risk professional, so I've been working in the fraud area for the last 17 years. Most of the time, I spent working for fintech companies and now I'm leading G2A, which is the largest digital entertainment marketplace in the world.

Yeah. My name is Iremar Brayner. I'm originally a Brazilian, but now I'm living in Portugal. I'm a fraud prevention and risk professional, so I've been working in the fraud area for the last 17 years. Most of the time, I spent working for fintech companies and now I'm leading G2A, which is the largest digital entertainment marketplace in the world.

How did you get into fraud prevention? Was there a specific event, or has it just been the natural progression of your career?

That's a very interesting question because my first job, I was to work for a bank and a customer service team, to be more specific about it. When customers were not happy anymore about the service, so they would call to cancel the services and everything, and I was one of the guys trying to convince them not to cancel the credit card or the bank account.

At certain points, there was a new area in the bank, and they were trying to be a department that would be responsible for speaking to foreign customers. I was promoted to that department, and after that, one of the responsibilities of that department would be to confirm and review suspicious transactions. By suspicious transactions, I mean high-value transactions or any transaction that would be normal for that specific customer. That's how I got into fraud, and yeah, it's been 17 years now.

I assume that you enjoy this field, and that's why you're still in it after 17 years.

Yes. I do like it a lot. I went to law school, and at certain point, I thought, “OK, I really like the law school. I want to finish. I want to get my degree, but I don't want to be a lawyer anymore, so I want to continue working in the fraud prevention area.” I got my degree, but I decided not to work as a lawyer.

But I'm sure that background of the way that you look at things because of the law degree impacts the way you view situations, I'm sure.

Yes, yes, it does. Because in the law school, you have a lot of psychological things, psychological classes, for you to understand how regulation is built and things like that. The relation between that and fraud is because fraud is normally attached to something emotional. I normally say there's an emotional side of fraud because people are more likely to scam or to be scammed when there's something emotional involved.

I normally say there's an emotional side of fraud because people are more likely to scam or to be scammed when there's something emotional involved. -Iremar Brayner Share on XFor example, if you're struggling financially or, for example, you really want to go to Oasis concert and you cannot get the tickets, what you do? You try to buy from secondhand ticket, but maybe that secondhand ticket is not real, it's just fake. But you're so happy about getting the ticket that you might be a little bit…you might not pay attention to all the details before purchasing the fake tickets.

Yeah, that's often where scams and fraud starts, is it's something that we're eager and excited about and we're willing to let our guard down a little bit and get what we want.

Yeah. Same thing happens with romance scams. People really think that, “OK, I just found the love of my life. If the person needs money, I will lend some money,” and things like that, but that could be really dangerous. The law background helps me to understand how fraud has always a psychological reasoning behind.

In your particular marketplace, what are the different types of fraud that you're working to prevent?

Yeah, so at G2A specifically, since in our marketplace, we focus on digital content, that could be attractive to fraudsters for different reasons. For example, some of the products available on the portal are really easy to cash out. For example, gaming gift cards or cash gift cards. It's pretty much cash that you can just, you got the gift card and then you just cash out.

Normally, the average price of our items is really low, and that could be also attractive to fraudsters because when fraudsters get access to stalling financials, stalling credit cards, they need to test it out before buying something more expensive. So what they could potentially do,

they can try to buy something that costs like $10 in our marketplace, and if it gets through, then they move to another marketplace to buy, for example, electronics.

That could be a little bit attractive to fraudsters, and what we've noticed that is happening right now, not only in our marketplace, but in the fraud scenario, generally speaking, is what we call friend with fraud. Over time, it's getting more difficult for fraudsters to commit fraud, to get access to stalling information and things like that.

What some fraudsters are doing, they buy things by using their own cards, and then they just call the bank and say, “Oh, it wasn't me. I do not recognize this transaction.” But they already got the item or the service they paid for, so this is something that is trendy right now for the whole industry.

Yeah. I suppose that any time that there's new products, there's something exciting, new to the market, or there's a financial downturn that that wasn't me, fraud increases.

In our platform, for example, one of the things that we sell are games for PlayStation, Xbox, and so on. I can give you an example. A lot of people around the world, they're really waiting for GTA 6, the game, to be released, and that's going to be released at the end of this year, if they do not postpone that once again.

We know that's going to be something really big, and of course, we are going to be ready to be able to prevent fraud, because that's going to be something that everybody is going to try to buy, is going to be attractive not only for regular users, but also for fraudsters, because again, if they buy it, they can easily make money on it. So those things, when there's a new game being released, is something big for our business, so we need to be ready to be able to manage fraud.

I mentioned you've got challenges from both sides of the equation. You have people that are fraudulently listing something that either they don't have, or it's a fake, or they're not going to actually deliver it, and then you have the buyer side who are going to pay with a stolen credit card, or things like that. How do you approach each of those types of potential fraud situations differently?

Yeah, that's a very good question. One of the challenges about managing fraud in a marketplace is the fact that you need to mitigate risk on both sides. I can give you, as an example, on the seller side, we have a KYC process to make sure that the seller is legit, that he or she is really going to deliver the service or the digital product they're offering, of course, and we also monitor the number of complaints that those sellers are receiving to make sure everything is OK according to our policies.

On the other hand, on the buyer side, we monitor all the transactions in real time. One thing, one decision that we made not recently, but some time ago, is we moved away from manual review, and that's something nice to highlight, because it's very normal for marketplaces to have manual review. Manual review basically means that you try to buy something and it needs to be reviewed by a human being to say, “OK, this is good or a bad transaction.”

Because of the nature of our business, we moved away from having manual review, which means that 100% of our transactions are automatically reviewed. We make the decision in seconds, really quick. And the reason why we've done that, of course, it will improve customer experience. User experience is way better. Again, imagine you're just like a 17-years-old boy that wants to play a video game and you're trying to buy a game online.

Then you get a message saying, “OK, we are going to review our transaction and then we'll get back to you in 48 hours.” You say, “No, I'm not going to wait for 48 hours. I'm just going to move to the competition and buy the game.” So, yeah, those are things we are doing. We've been doing on both seller's side and buyer's side to make sure we have a safe, but at the same time, a platform that provides a good experience for both sellers and buyers.

Yeah, and that's one of the challenges that I'm hearing more and more frequently is we've gotten with society to this place where we want frictionless transactions and we want instant gratification. As soon as I hit buy, it's in my inbox where the package is already shipped out the door, but that doesn't lend itself well towards fraud prevention.

And so it's trying to find this balance of how do we do good fraud prevention, but also, like you said, maintain good customer service. Also, when you're trying to balance it between your own financial interests of we can't have 50,000 employees looking at every single transaction, particularly if they're low-dollar transactions.

Exactly. It's a very tricky game because you need to kind of balance user experience and financial results, of course. And we've been working a lot on automation and AI to increase the efficiency of our operation. And again, this is key in our business model because our users, they really want things to be really fast, but fast in an efficient way. We've been working a lot on automation and AI and reviewing our policies to make sure we are efficient and safe as a platform.

As you started to introduce AI into your order review process, has it uncovered anything unexpected? Has it come across, “Hey, AI, we found this whole new concept of fraud or this new pattern that we'd never seen before,” but the AI was able to find it?

I love this question because when I hear people talking about AI, it kind of sounds that, “OK, fraud is going to completely change. We're going to find out new things that they were never seen before.” But, actually, what AI is doing on a fraud side is just making fraud more scalable. So fraudsters, they need less effort to do something really big.

But, actually, what AI is doing on a fraud side is just making fraud more scalable. So fraudsters, they need less effort to do something really big. -Iremar Brayner Share on XAnd I can give you an example. Like social engineering was always there, but now it is just done in a different way. For example, I remember like 10 years ago, I used to work for a bank and people used to receive phone calls from people claiming they were the bank representatives. “Oh, I'm calling from the bank. I just want to help you to have a higher credit limit. And if you provide information A, B, and C, I can help you with that.” That was 10 years ago.

Now the same thing has been done, but through social media. Like fake social media accounts, they were created in order to get sensitive information. And after that, they can use that sensitive information to steal money from your bank account, a credit card, and things like that. The scams are the same pretty much, but the way it's just more difficult to tell whether something's true or not, that's number one.

The scams are the same pretty much, but the way it's just more difficult to tell whether something's true or not, that's number one. -Iremar Brayner Share on XAnd number two is way more scalable now to commit fraud because of the technology. But on the other hand, we can also use AI against AI. Another question that people have been asking a lot is, “OK, now with AI, does it mean that we don't need manual intervention anymore?” And that's not what we believe, especially at G2A. What we believe is that AI is helping us to automate what can be automated, what should be automated.

But especially when it comes to fraud, there's always a human touch. So we're going to use AI to automate what needs to be automated. And we are going to continue using real people to do what only people can do. So long story short, the way we see AI at G2A is it's going to be a war between AI against AI plus human.

But especially when it comes to fraud, there's always a human touch. So we're going to use AI to automate what needs to be automated. And we are going to continue using real people to do what only people can do. -Iremar Brayner Share on XYeah, and I guess when you're in your scenario where you are a platform, if someone is trying to exploit AI to, let's say, buy a whole bunch of products or sell a whole bunch of products, you'll see that, in some sense, if your sales double or the product's being listed double overnight, that alone is something suspicious unless GTA 6 is launched. But sudden changes become very noticeable when you have a large platform.

Yes, yes. In the past, fraud managers, they would focus on fraud rate, chargeback rate, payment approval rate, payment decline rate to check if there was something wrong. But now we are actually monitoring what happens before that. So let's suppose that there is a 200% increase in sales for a specific product. And there's no sales campaign about it. It's not a new release. It's completely out of the blue.

This is something that we're probably going to have to stop and check what's going on. Even though there's no fraud reported yet. So yeah, I totally agree with you. Sudden changes in the volume of transactions, it's something that we definitely are looking at when it comes to mitigating fraud.

If there's a little switch detail that you can't answer about this question, I understand. How do you mitigate against money laundering in your situation where you have people selling gift cards and buying gift cards of, “OK, now we're exchanging monetary products for monetary products”? How do you mitigate the risk of money laundering?

Yeah, of course, I cannot disclose all the details, but generally speaking, there are different ways that can be used to mitigate money laundering. Normally, what international companies do in order to follow the payment system regulation, we try to make sure that the person that is buying or the person that they sell is not sanctioned in a way. This is something really, really basic.

Another way of mitigating that is that setting limits when it comes to how much items or how much money you can spend, like daily, weekly, monthly. And normally, companies do not have one single approach for their whole volume of transactions. If we know that one specific product or one specific segment product category is riskier than others, of course we're going to take additional measures to make sure that we are able to mitigate that risk.

That's pretty much what companies are normally doing too. And if they found out something shady when it comes to money laundering, like the natural flow would be to report transactions to authorities if necessary, or to ask for additional information, to ask the customer or the user additional information. “Oh, we would like to understand why you're trying to buy, like, 200 gift cards in 24 hours.” That's probably something wrong. And being wrong doesn't necessarily mean that it's related to fraud. That could be something else.

It's just unusual enough to catch your attention.

Exactly, exactly.

And so if you've worked in multiple industries, what are some of the different ways that you've managed fraud in different industries or that fraud presents itself in different industries?

Yeah, again, very nice question. I remember some of the challenges I faced working for some specific industries. I used to work for a ride-hailing company. So, ride-hailing company is pretty much a car service that is going to take you from point A to point B.

And when I first started to work for that company, and I was like, OK, to me, it's kind of obvious how to mitigate fraud if you worked for a bank. But what could happen? Just a person requesting a car to take you from point A to point B. And it was really interesting to understand how the fraud techniques vary in different industries. For example, in ride-hailing, it was very normal. People abusing—especially drivers abusing sales campaigns or incentive campaigns.

Let's suppose you are a driver, and then we just send you an email saying, “OK, if you indicate 10 drivers or one driver, we're going to give you $100 extra money.” What some people would try to do, they would indicate themselves. They send a link to themselves. They try to create another account and a second account and a third account and a fourth account. They are not indicating new customers. They were indicating themselves.

That would be something really normal for that industry. On the same note, sometimes, in order to be a driver, you need to have a valid driver's license. Some people just didn't have a driver's license. What they would do, they would try to rent someone else's driver's license in order to drive. It's a different type of fraud, but it's still a fraud. And I think that was…

With any consumer, stolen credit cards is probably high on the list.

Yeah, exactly. On a passenger side, the most common thing would be people use installing credit cards to pay for the ride. That’s normal. But it was tricky and challenging, but also interesting to me to understand how the fraud dynamics worked for that specific industry.

Were there also issues of people signing up and then they weren't actually the driver? It was, “We're going to sign someone up and there's just going to be actually just an entirely different person driving.”

Yeah, yeah, that would happen. That is linked to the example I gave you about person driving and using someone else's documents. And then there were some techniques to kind of identify that. So you, as a passenger, if you see that the person that is driving the car is not the same you see on the app, you can report it.

And then we would start to investigate it. Or if we think that there's something suspicious about the driver not being the person that he's claiming to be, we would trigger things like face recognition. You need to show your face, so then we compare your face to the document we have on record and things like that.

Yeah, I've definitely, as a passenger, I've definitely experienced the wrong driver, that Bob was clearly not Bob. And then let's see, I've also experienced, I had one driver say, “Oh, I'm not driving my normal car, I'm driving this other one instead.” And I'm like…

That's probably an excuse.

That wasn't a media, so it won't be the license plate that the app says. I'm like, “OK, I'm canceling that one right away. That's already very concerning.”

Exactly, yeah. And yeah, but that was really interesting. I have also the opportunity to work for a different marketplace, but that was focused on luxury items, especially expensive bags, jewelry, clothes, and things like that. And it was really challenging because the average value of the transaction was really high. And the audience that normally buy those things, they have some—it’s a very unique type of customer that buy those things.

And sometimes you need to ship a watch that the person's paid $100,000 for it. And then there's a special procedure to make sure you're really going to get the item and it's not going to get lost on the way. So yeah, that was also an interesting experience. It's still high risk, but again, I've learned a lot from working for these different companies and different segments.

What would you recommend to consumers, not necessarily specific to your platform, but when you're doing online purchases? If I'm going to buy a $100,000 watch from someone I've never met before and I'm going to do it entirely online, to me, that seems really scary. If it were something in person, I would want to meet at a trusted watch dealer, be able to confirm that it's legitimate, that the watch is really what it's supposed to be. But you can't do that online. What are the steps that consumers should be taking, whether it's a large ticket item, $100,000 watch, or a $20 game?

I would definitely recommend people to buy from reliable sources, especially if you're buying something that is really expensive. I would also recommend to check the refund policy. Because if you're spending a lot of money, even if it's not a lot of money, but buying something, you need to make sure that if you get the item, is not what you wanted, you are able to return it and get your money back.

Something that is basic but still works is make sure the price makes sense. Because it's very normal for people to buy something that is really, really underpriced. And then they get the items, not what they were waiting for, and then they complain. But sometimes there's no refund policy, so they kind of lose the money. And do not share your credentials or personal information with anyone. Those are really basic things. But believe me, they still work. They still work.

And on the seller side, what are some of the things that they can do to prevent someone from claiming that, “Oh, well, I ordered this, and this isn't really what I got. It was broken, or it was just a brick inside of a box”?

Yeah, one thing that makes a lot of difference on the seller side is you need to be really accurate when it comes to the item description. “OK, this is what I'm selling. These are all the details, colors.” If it's a secondhand item, “Oh, it has some scratches,” and things like that. You need to be very, very accurate when it comes to the item description.

If you're selling something that is physical that you need to ship, make sure you have all the tracking number, all the shipping information, because if the buyer claims he or she did not receive the item, you have a document to say, “OK, here's the document. I shipped this item like two days ago. And we can try to get in touch with the shipping company, but there's nothing I can do right now.” I think I still believe the most important thing is to really focus on how well the item you're selling is described on the portal.

Is that most of the complaints through—clearly, now you're doing mostly electronic stuff, but for physical goods, is that often one of the more common complaints on secondhand items is that it's just not in the condition that it was advertised in?

Yeah, if you're not considering the fraud scenarios, like people use installing cards and things like that, most of the complaints would be related to one, I did not receive the item. And sometimes this complaint is actually not accurate. Because if you buy something, if you're selling something, and you ship the item, and the item was not delivered to the buyer, a lot of things could have happened.

The item could be lost on the way. Maybe there's a fraud scam between the company that is delivering the item and the person that is supposed to receive the item. That would be number one, item not received. And the second would be item not as described. And normally, item not as described in a normal scenario is related to the fact that the item was not described well. Those are the most common scenarios.

Gotcha. And because we've been talking about fraud for a while, I do like to ask my guests that are in the counter fraud and the counter-scam space, if they've ever been a victim of fraud or a scam. Because I really want to destigmatize the experience of someone being a victim, that if you and I can't get it right 100% of the time and we live and breathe in this space, that people who don't spend their days thinking about fraud and thinking about scams, if they get taken advantage of, if someone steals from them or they're a victim of a scam, they shouldn't feel that they're stupid. They shouldn't be humiliated. But the more that they share the experience, the more that it helps everybody else. Do you have an experience that you can share?

Yes, yes. I totally understand what you've mentioned about people feeling bad about being victim of a scam and not people struggling to share that, because they are really afraid of being judged somehow. But I think five or six years ago, I was victim of fraud. I was just with my phone, and then I just got a push notification saying, “Oh, a $2,000 transaction was approved on your credit card.” And that was related to a flight ticket. And I was like, “No, it wasn't me.” I just reported the transaction to the bank. And after two days, the bank got back to me saying, “Yeah, we have investigated it, and it was fraud.”

And then you might ask, “So, what happened?” So, probably I bought something in a website that was probably a victim of a cyber attack. And then that's how fraudsters got hold of my credit card information. That's scenario number one. Scenario number two could be maybe fraudsters got access to a bunch of credit card information. And there's a lot of ways to do that. They just sold my information on the dark web. Somebody just bought it, and that's how it happened.

There's another interesting scenario. The fraud was not successful, but it was an attempt. I was at home with my mom a couple of years ago. And then my mom got a WhatsApp message from a person claiming to be me using my picture saying, “Hey, mom. This is Iremar. I'm struggling with my bank account. Can you transfer me $100?” And my mom was right by my side. And she said, “Yeah, did you send this message?” I said, “Mom, it wasn't me.”

I'm right here. I would have asked you in person.

Exactly. And that's one type of social engineering, especially if you receive a message from your kid saying, “Oh, I need that money because otherwise…I just need that money.” A lot of people would potentially transfer the money right away. What I told her is that, “Mom, if you are not sure whether that's me or not, or if it's something that I really need, just give me a call and then we can clarify things.”

If a person is asking money to you, it doesn't matter who the person is. Just do not transfer the money to you. Actually talk to the person, hear the voice. I know that voice can be manipulated as well, but just call the person and try to understand what's going on.

That's pretty interesting that your mom got that message, that it wasn't just a random number, but they had actually associated your face with that account that they created. So it was actually quite, in a scary way, quite targeted.

Yes, yes. And actually, I know a lot of people that experienced the same, especially now with social media, LinkedIn, so people can easily find a picture of you and just create a new WhatsApp account, add your picture, and say, “Oh, this is Chris.” That's one of the bad sides of social media, because we can easily get a picture of a person.

Yeah, yeah. But they knew to target your mom with your picture.

Exactly.

As opposed to—I have definitely had multiple friends or acquaintances whose social media accounts have been compromised, and their existing account was used to try to perpetrate that same scam. But it wasn’t—I guess I've seen it with brand new social media accounts as well.

Yeah, yeah. And sometimes fraudsters, they will take over your real WhatsApp account. Of course, if that happens, it's way more difficult to identify that it's a fraudster, it's not the real person. And after that happened, I also suggested my mom to activate the second factor of authentication that will prevent people from actually taking over her WhatsApp account. That was not the case, but that could happen as well.

Talking about two-factor authentication and your mom, and not to put you or your mom on the spot, have you found it difficult with older people or younger people in your life to try to get them to enable two-factor authentication?

Yes, I think that's the issue that we have in the industry, generally speaking, because not everybody is 100% familiar with technology on how to authenticate everything and things like that. I still know a decent number of people that still prefer to go to a bank branch to solve all the issues instead of giving them a call or trying to solve the problem by using the application. In a way, those solutions should be more user-friendly in a way, especially having in mind that not everybody is on TikTok, Instagram, and knows everything about technology.

Awesome. Any parting advice for anyone who is listening in terms of either helping to prevent fraud or if they're interested in getting into a fraud prevention field?

I would say that working in fraud prevention, it's something really interesting because it's a never-ending learning journey. There's always something new. We don't have a lot of fraud professionals out there, so that's good in terms of finding a job. If you're curious, if you like innovation and you like challenges, I think fraud prevention is for you. And just one side note about it: A lot of people ask me, “OK, I want to get into fraud prevention, so is there like a university that I should go to or something like that?” And the answer is no.

Of course, there are some courses you can take for very specific things. If you want to be specialized, for example, in 3DS authentication or KYC or compliance, but specifically for fraud, we still don't have a normal education flow that you should get into. It's more by experience. A lot of people just started like me. They were working for a bank as a customer service representative, and then out of the blue, there was an opportunity applied for, and that's how everything started.

Awesome. If people want to connect with you, how can they find you online?

Yeah, they can just text me on LinkedIn. I just look for Iremar Brayner. It's I-R-E-M-A-R. Brayner is B-R-A-Y-N-E-R. And yeah, I'll be there.

And we'll make sure to link that in the show notes as well. Iremar, thank you so much for coming on the podcast today.

It was really nice speaking to you, Chris. Really nice, thank you.